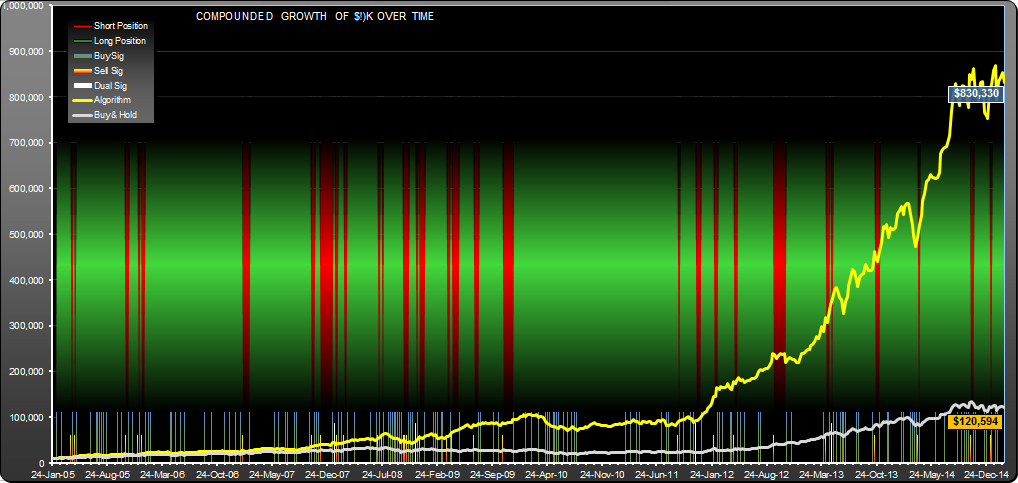

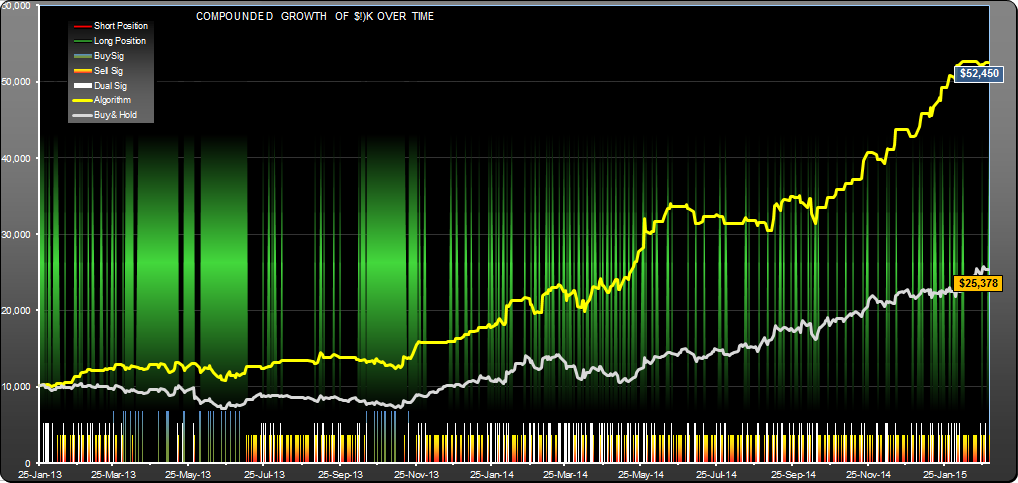

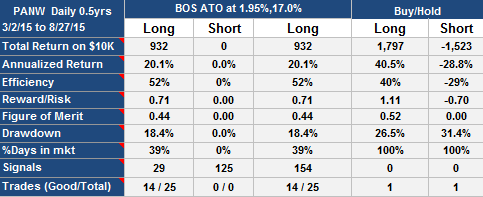

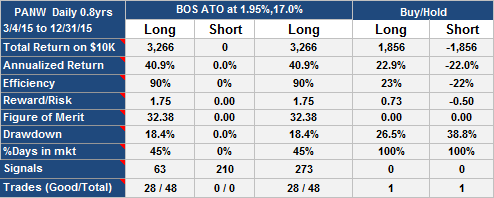

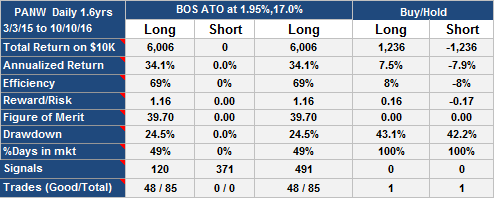

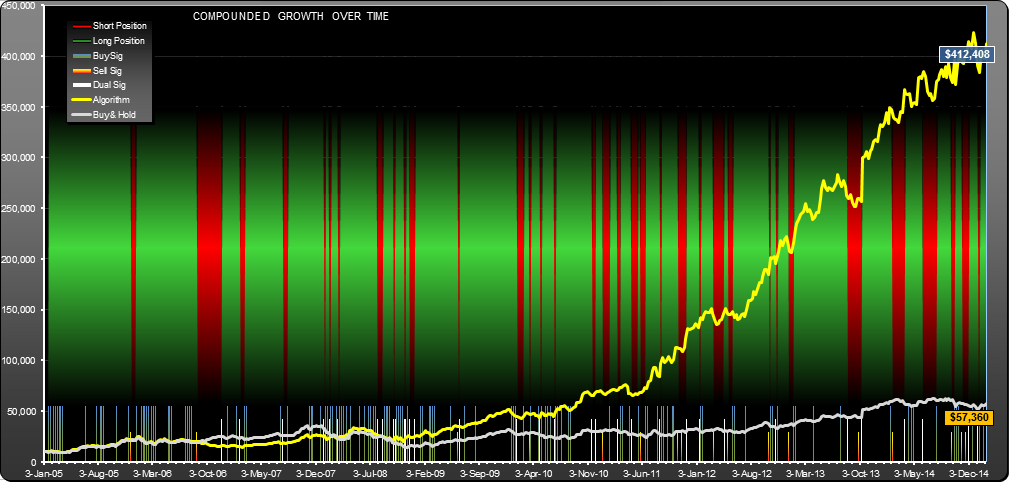

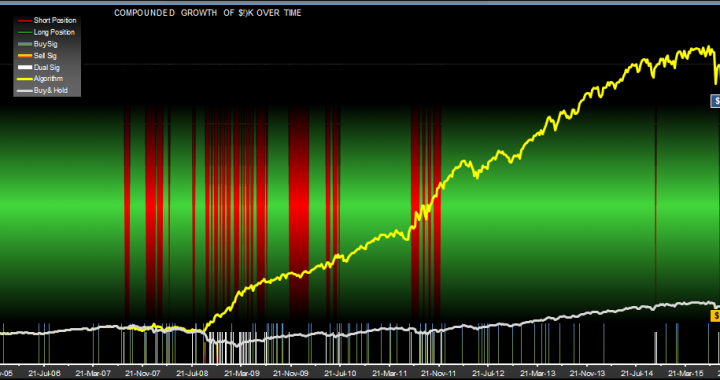

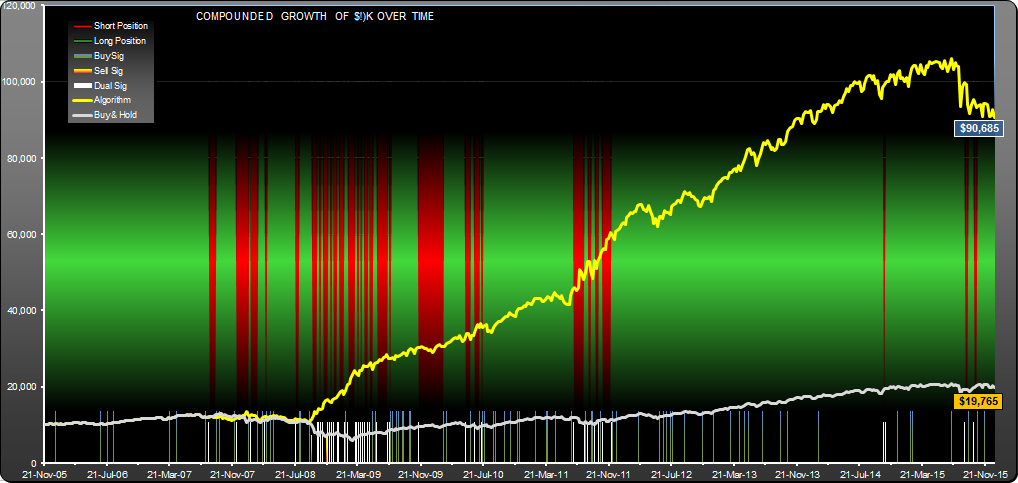

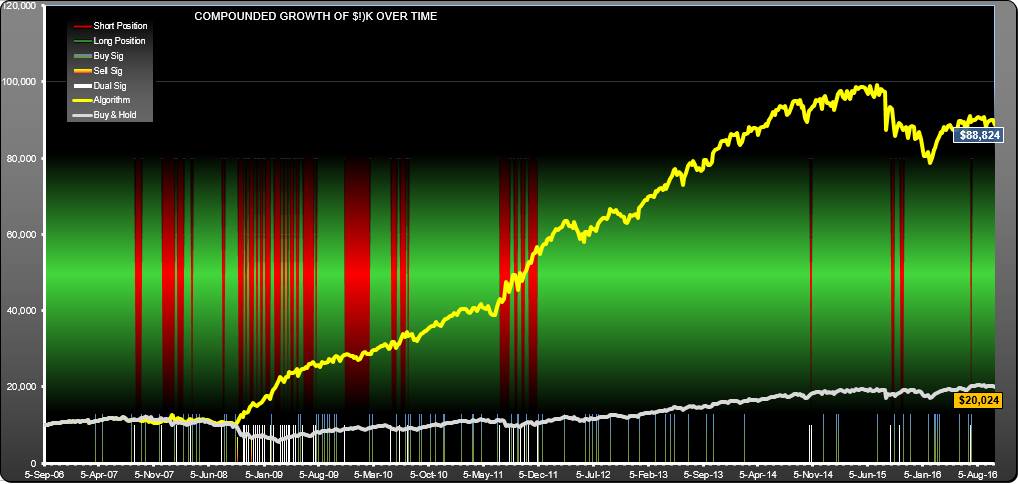

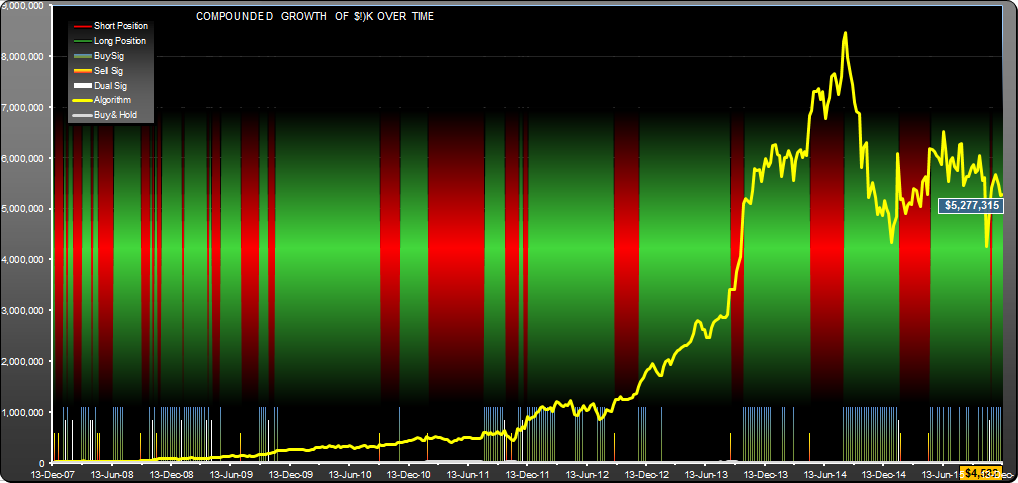

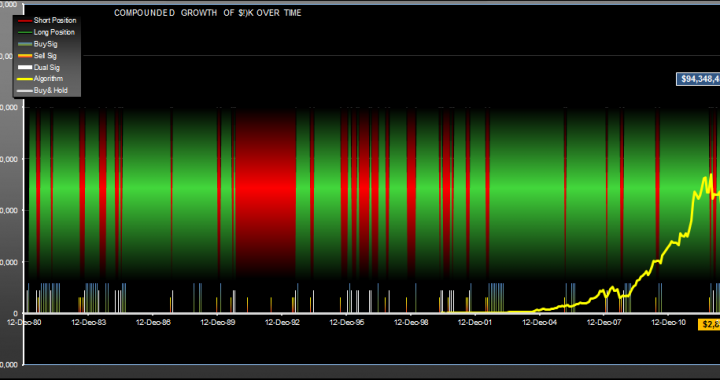

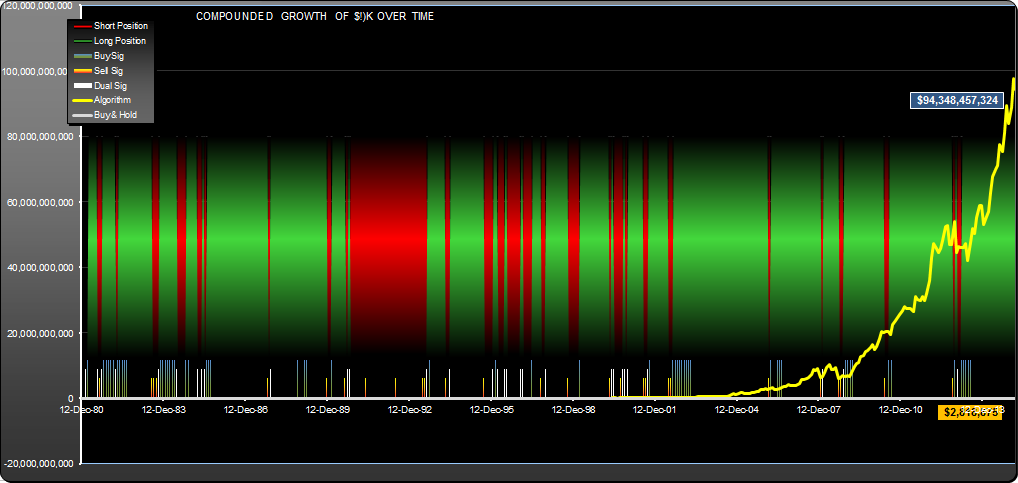

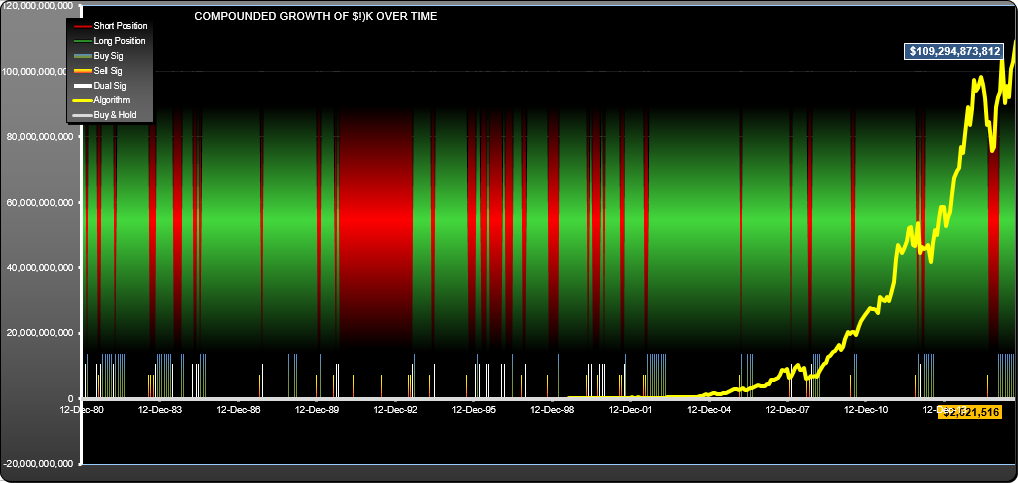

With $94 billion in profits (for $10K initial investment) this has one of the highest total returns I have seen for any algorithm.

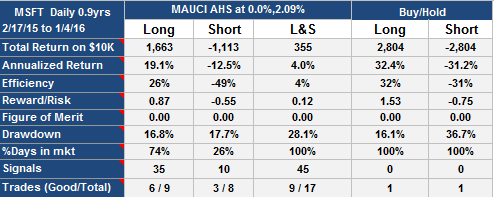

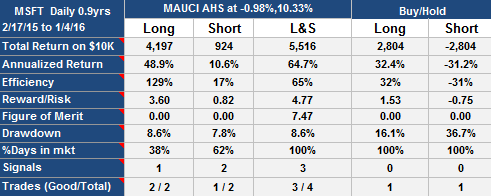

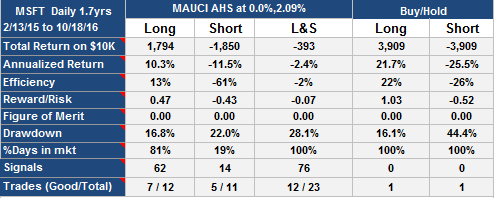

It is an interesting study, but I wouldn't recommend it as a good system to trade moving forward. It is somewhat over-tuned, and the parameters are close to regions which would have failed. At one time the equity went negative and you would have required extra capital to satisfy margin calls. The algorithm uses the "last sell price" as a reference. This can lock up an algorithm if the stock price is trending, in this case starving it of buy signals if the buy and sell percentages were chosen wrongly.

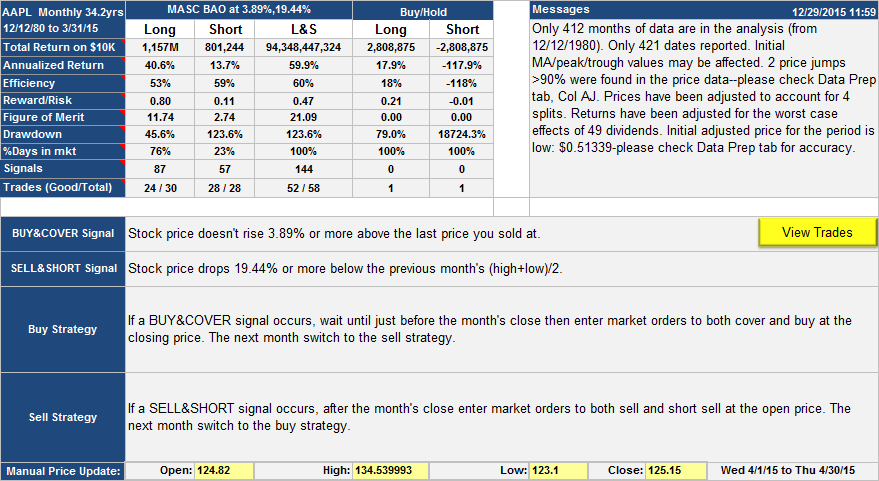

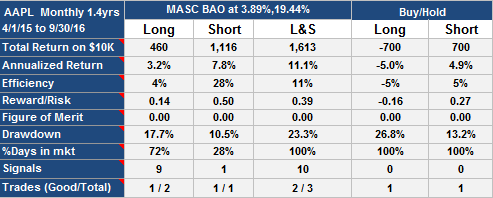

That said, I've been watching it for a year or so and it has behaved itself. The one take-away that you might find valuable--if you are holding AAPL and you see that portentous 19.44% or more price drop in a month, maybe you should take heed and sell at the next monthly open. The 29 times this happened over the last 34 years, you could buy at a better price later on.

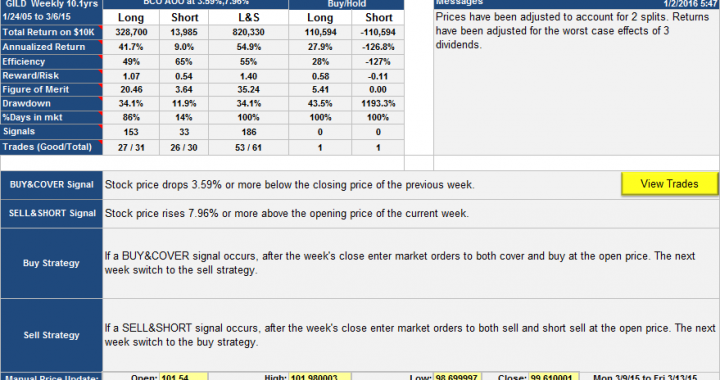

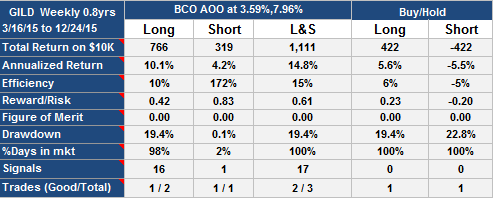

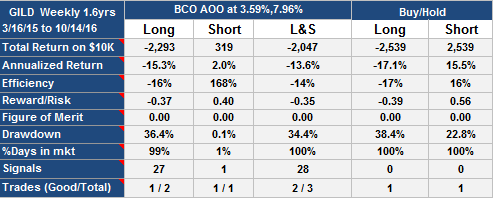

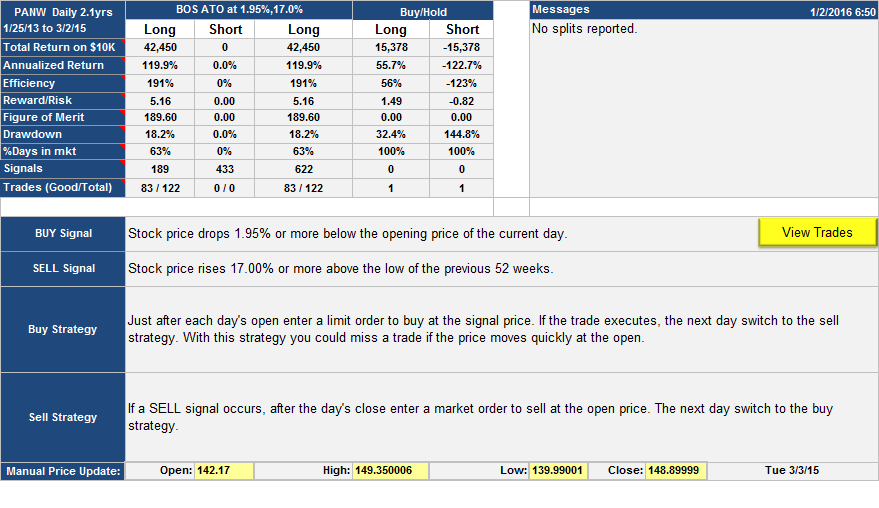

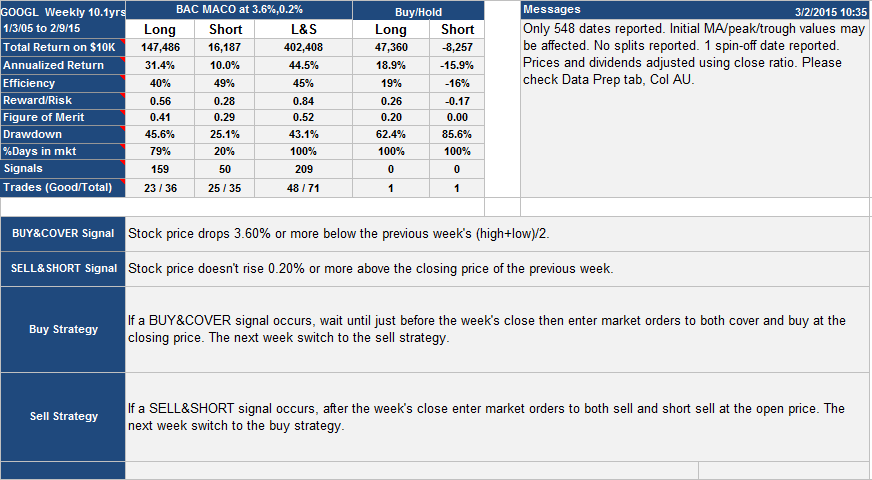

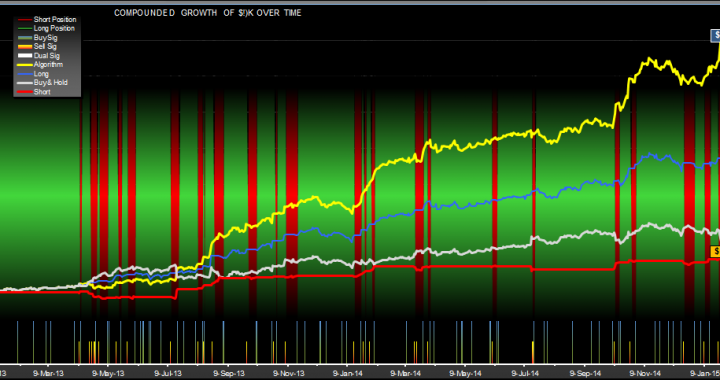

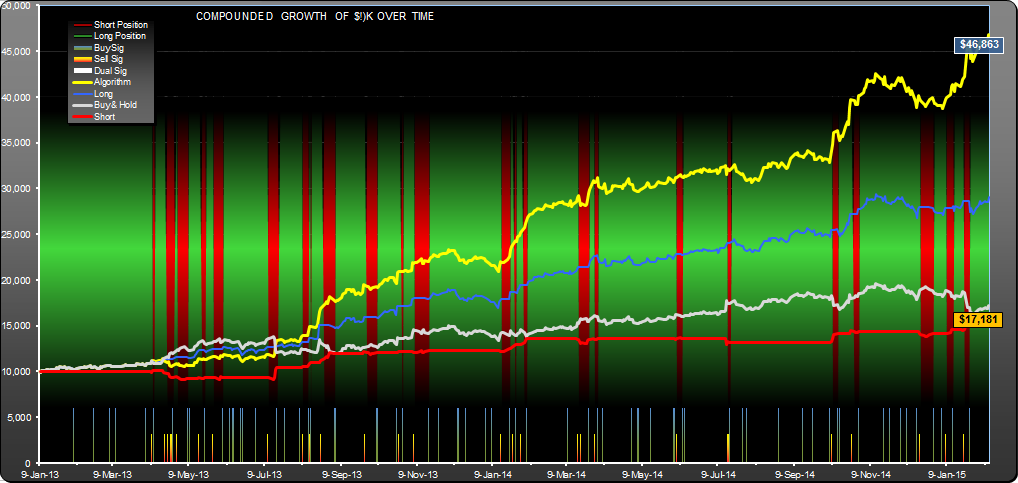

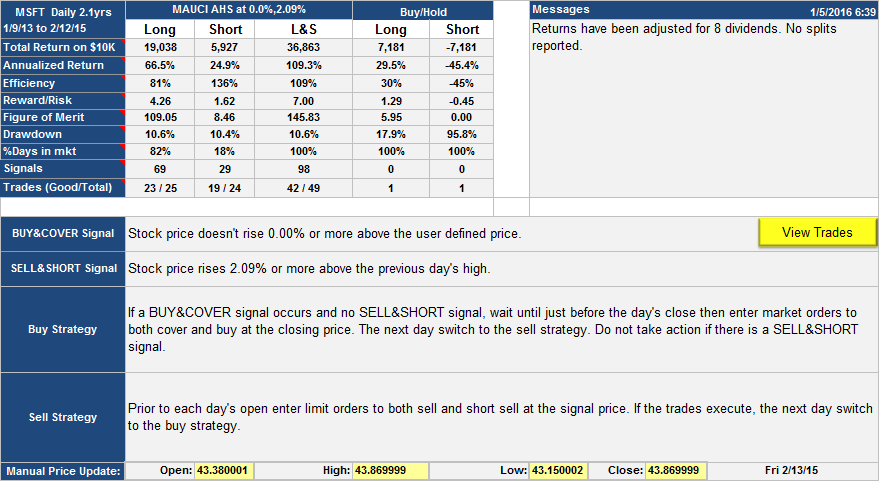

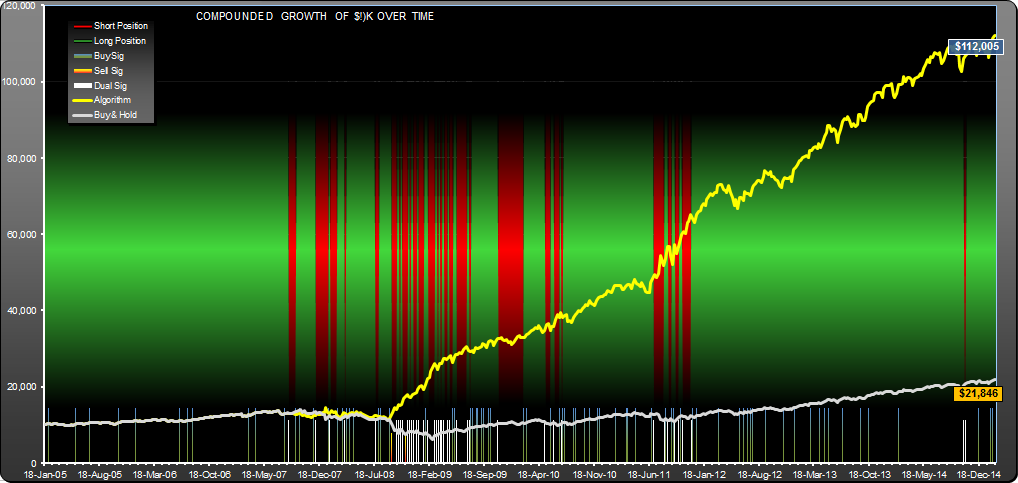

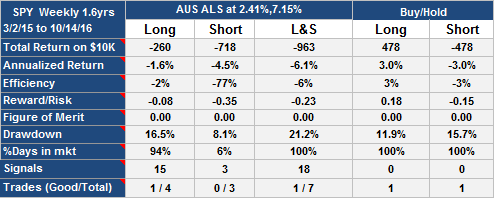

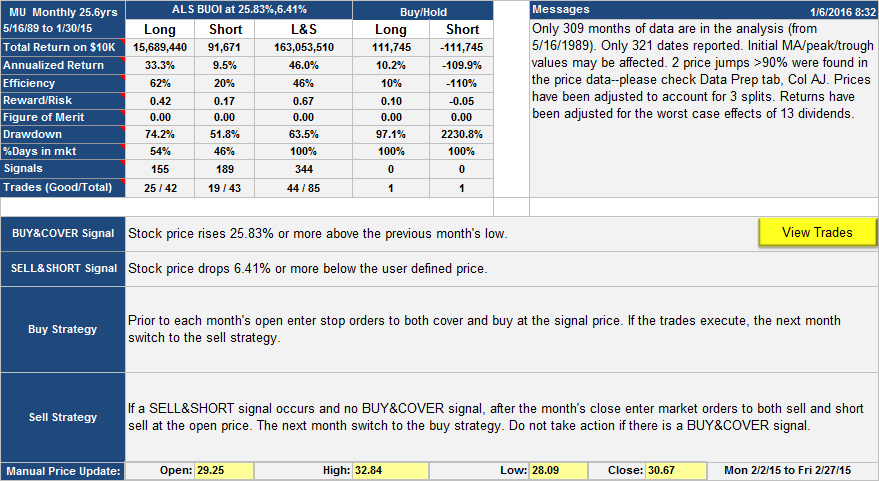

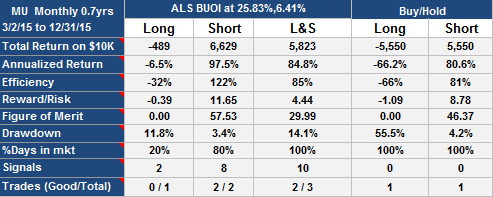

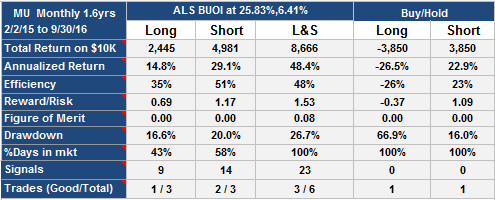

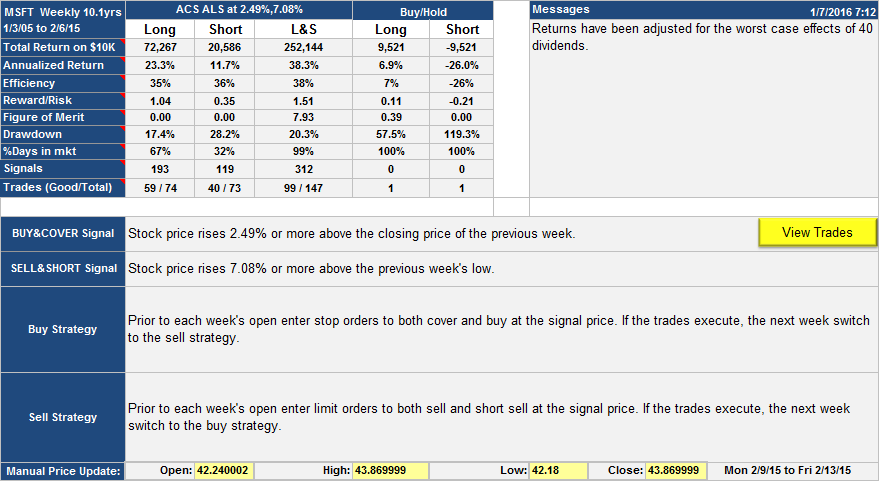

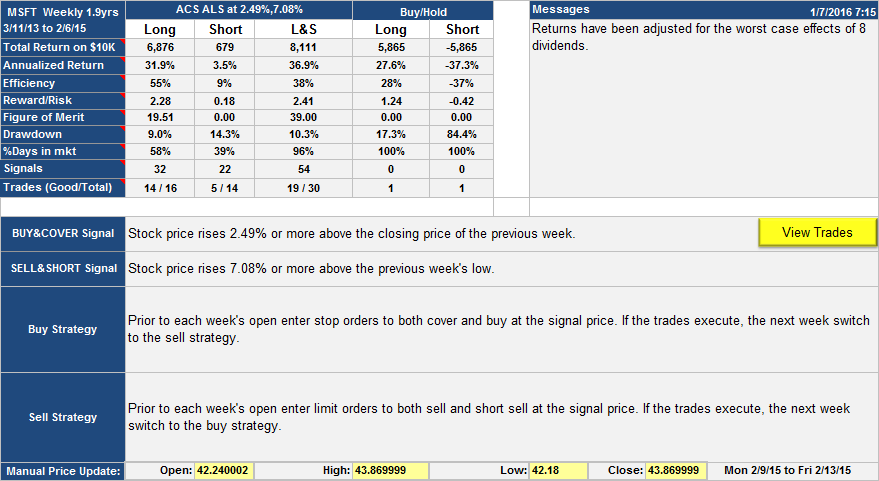

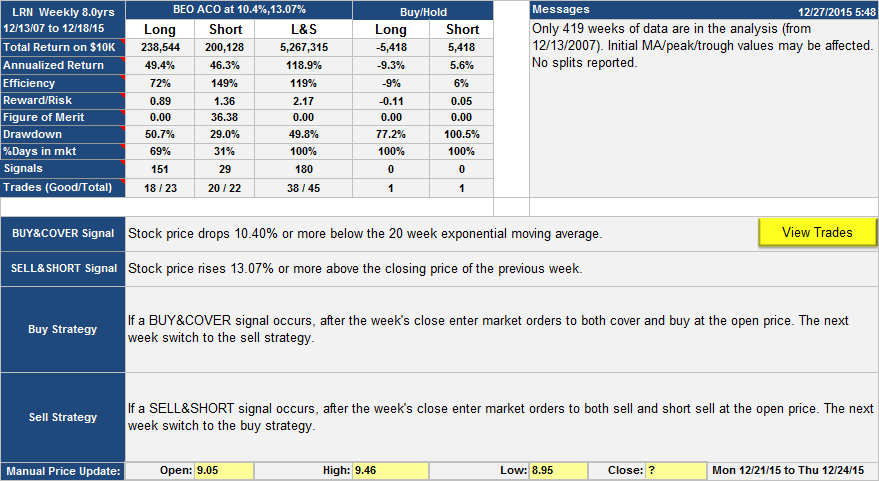

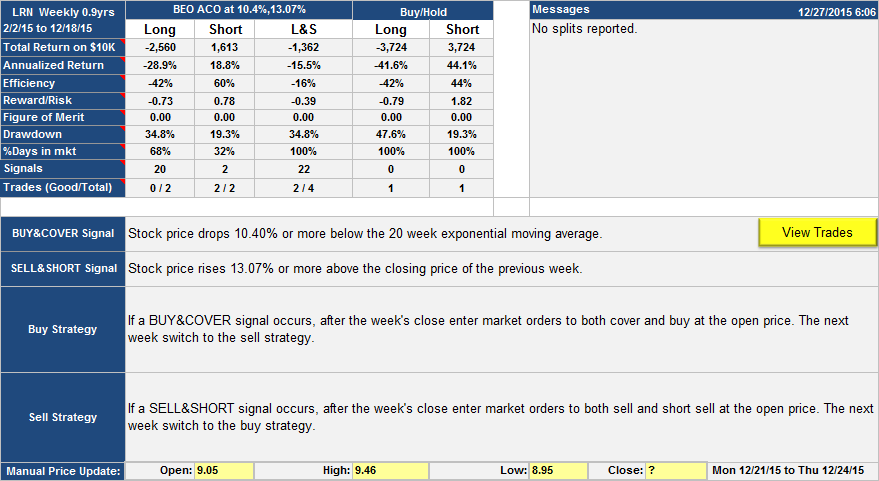

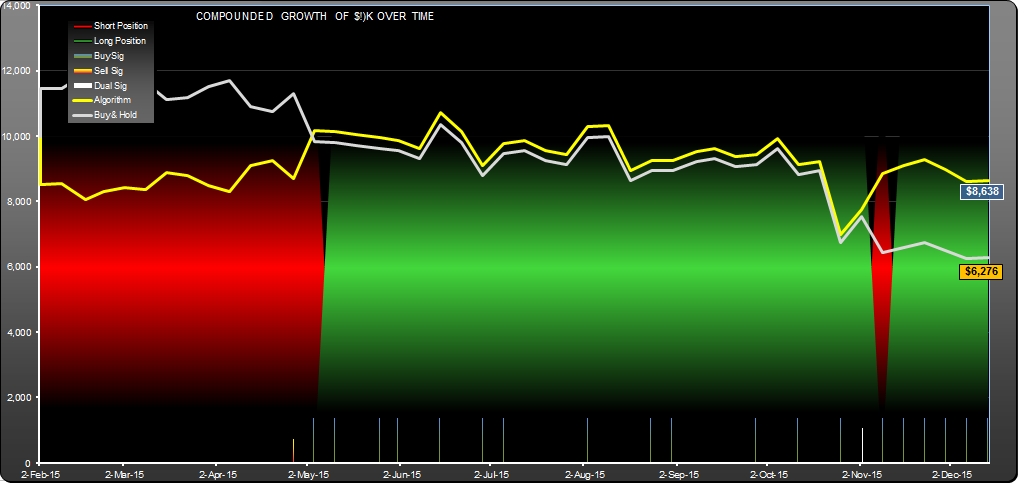

Notes: returns are compounded, commission was $7 per trade. Here is a list of trades: AAPL.M Trades

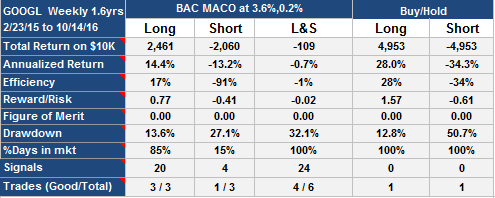

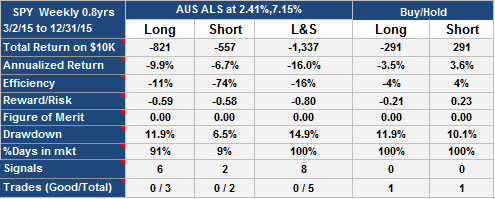

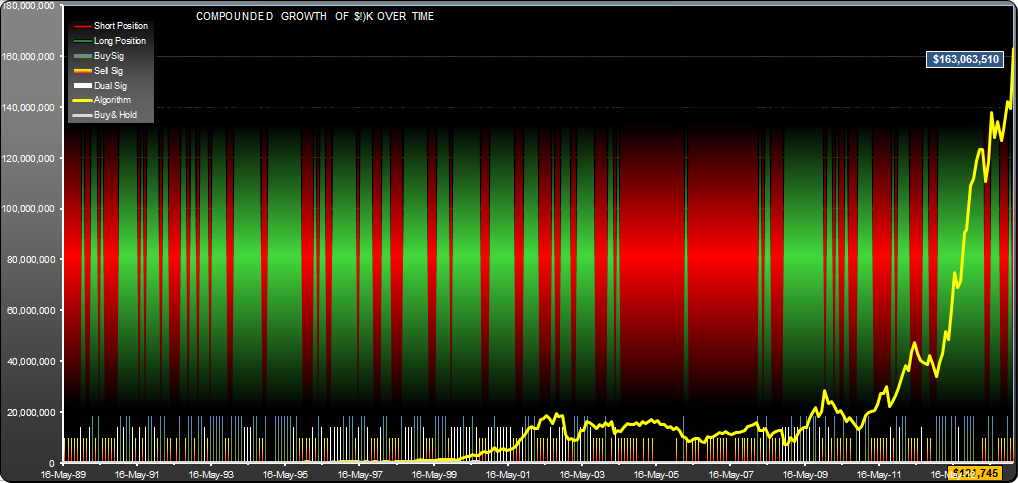

Note that the short side of the algorithm has a drawdown of 123%. If you look at the trades, you will see that this corresponds to a peak of $833,000 in Oct 90 and a trough of -$196,000 in May 91. This can happen on the short side of an algorithm, and would have led to expensive and quite possibly disastrous margin calls. The algorithm, however, recovered the following month when the stock price fell dramatically. The long side of the algorithm made $1,066,052,956 with only $10K at risk.

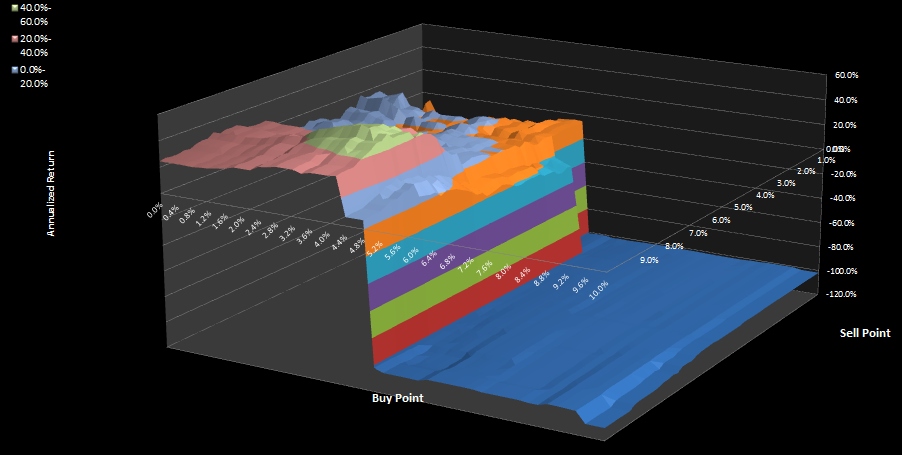

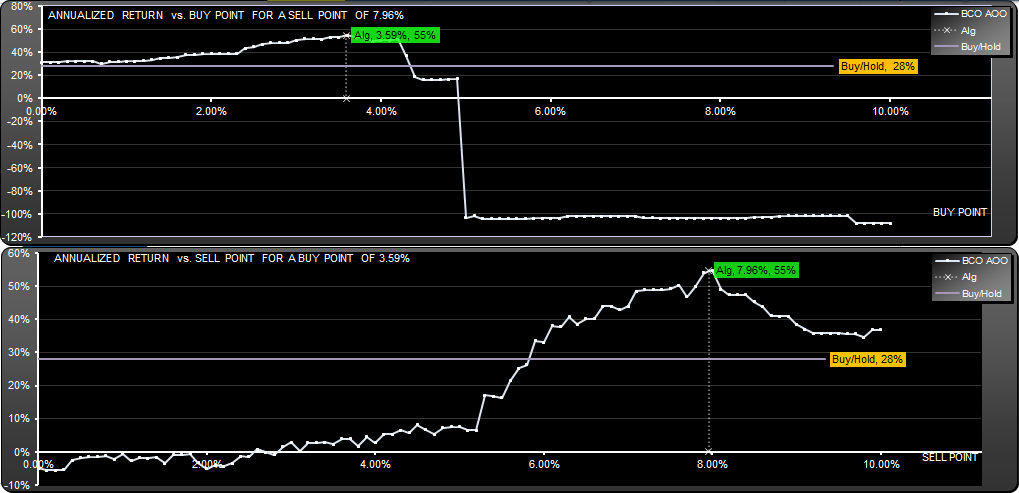

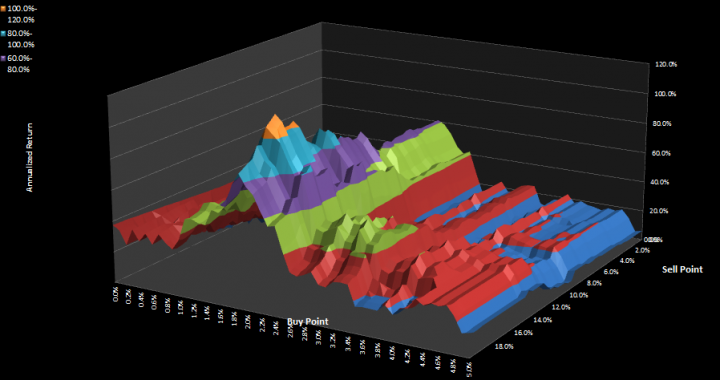

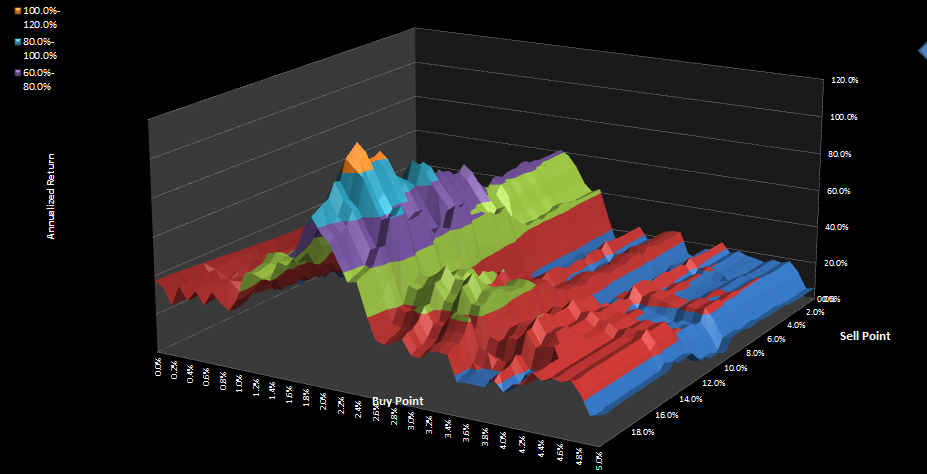

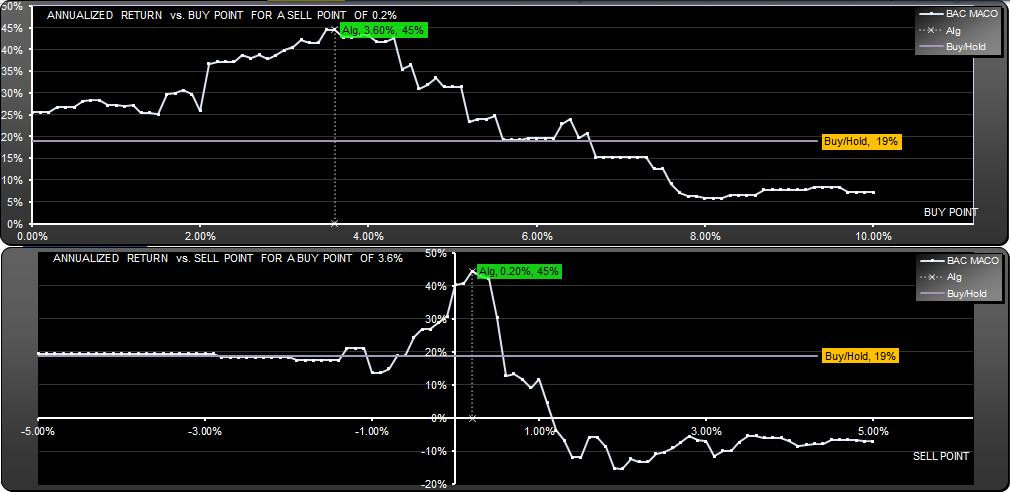

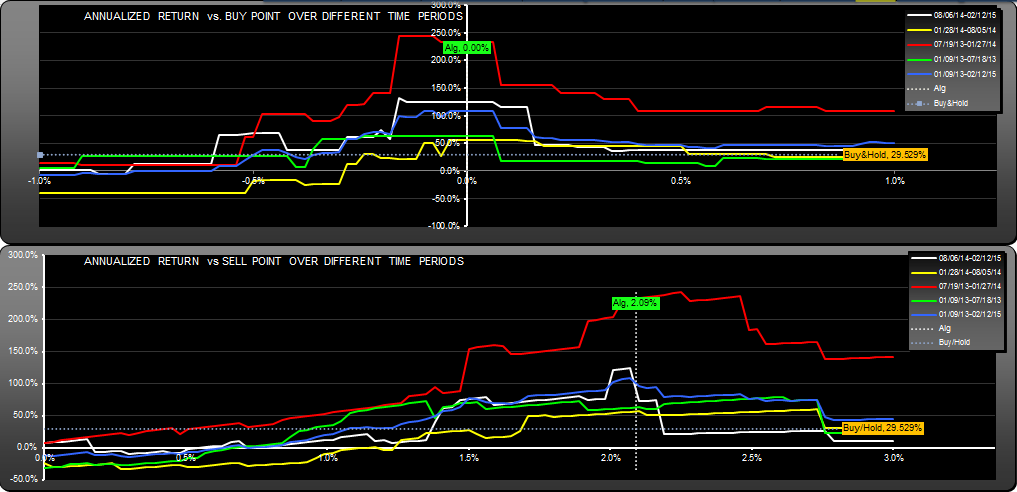

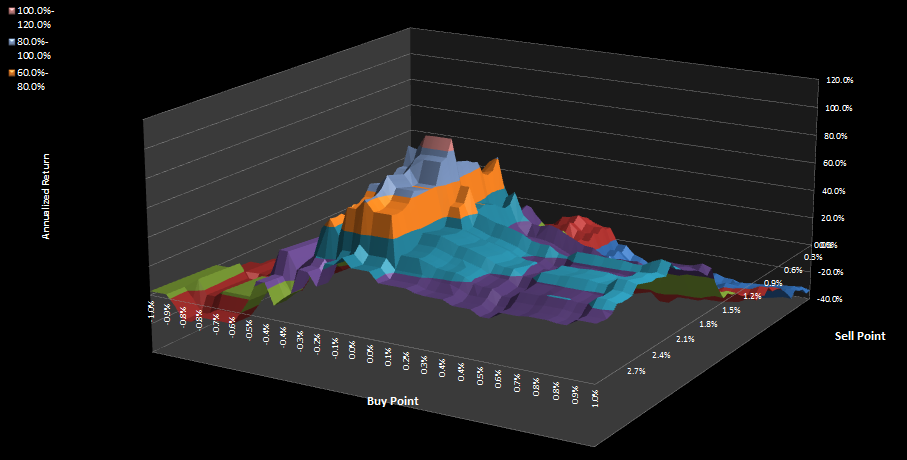

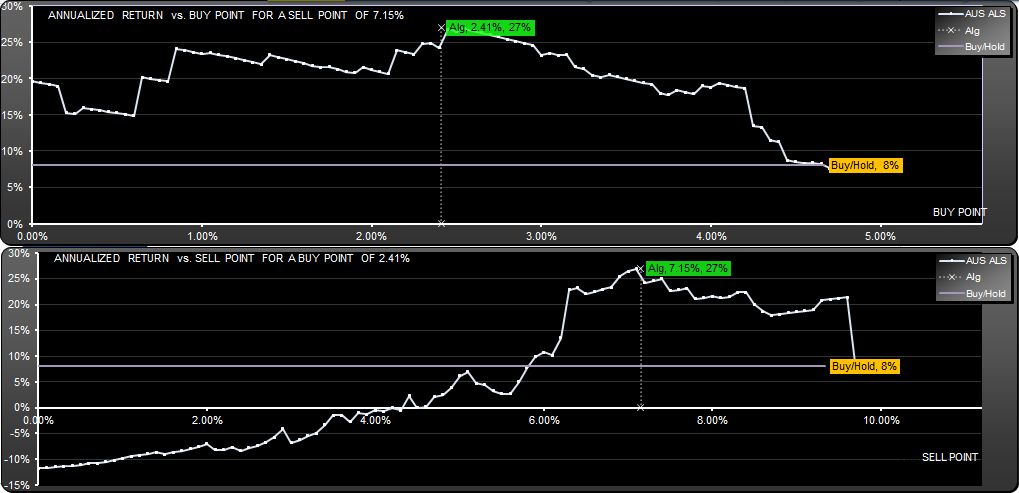

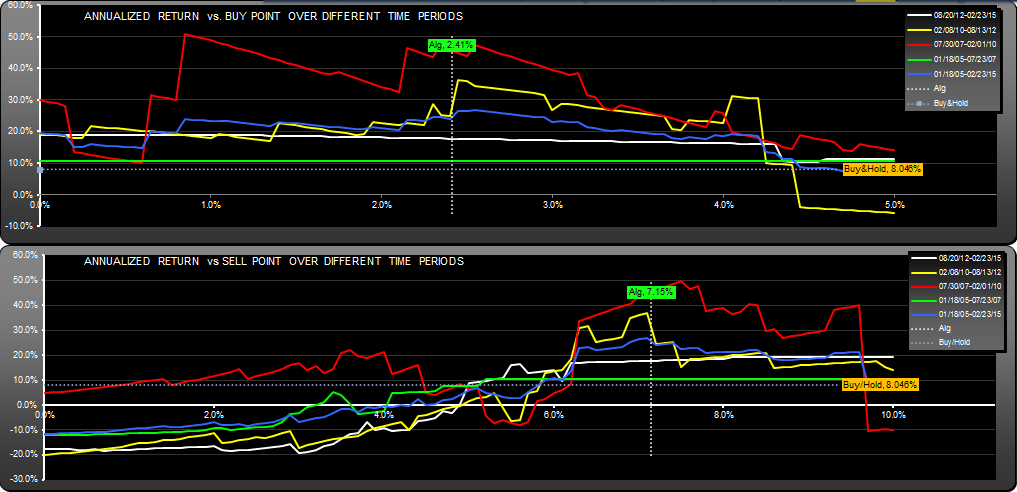

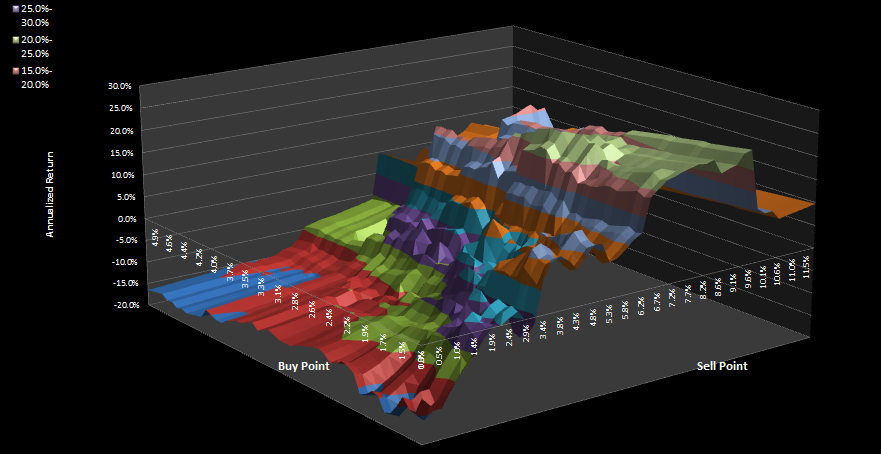

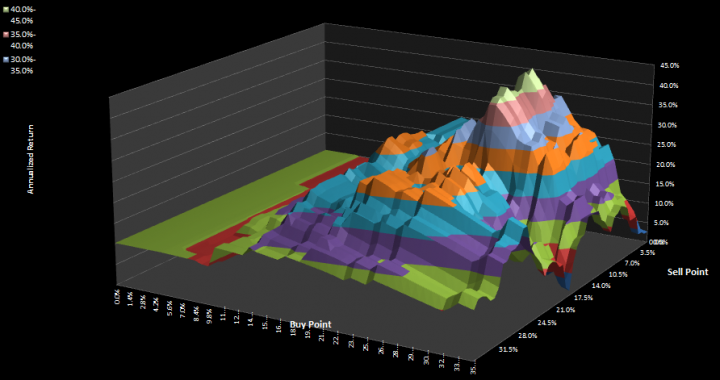

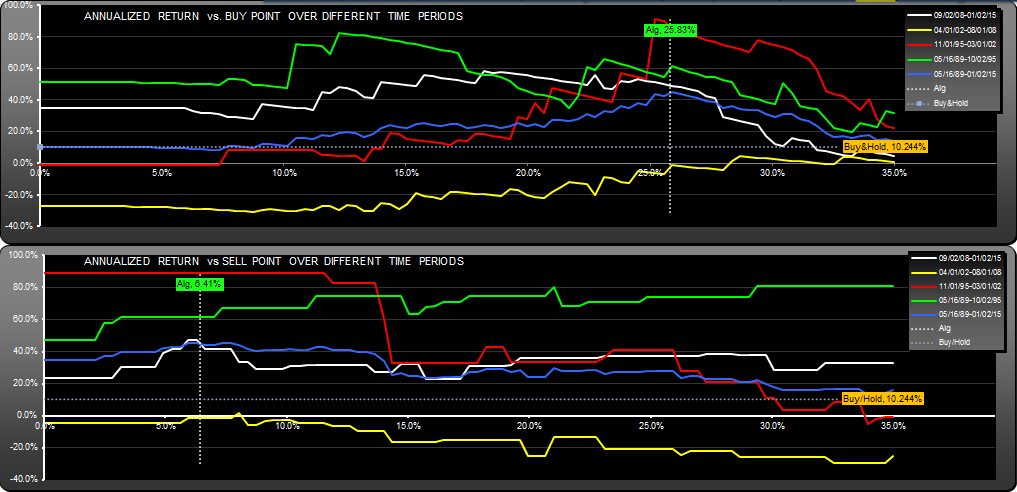

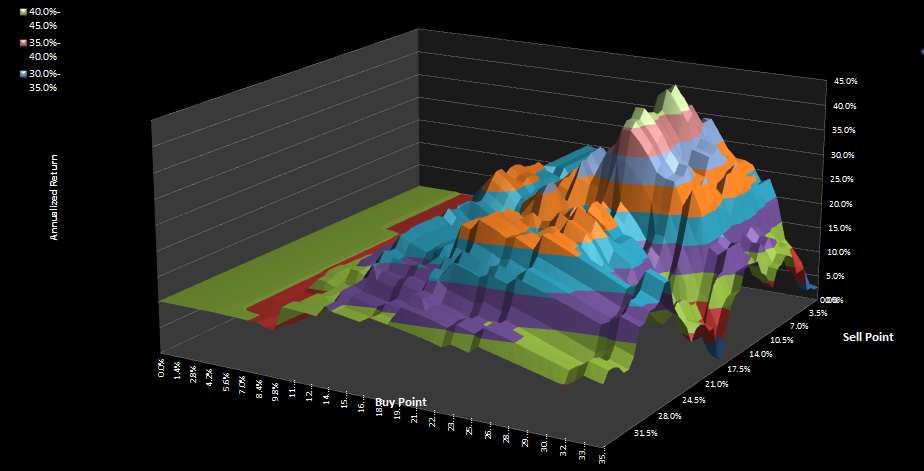

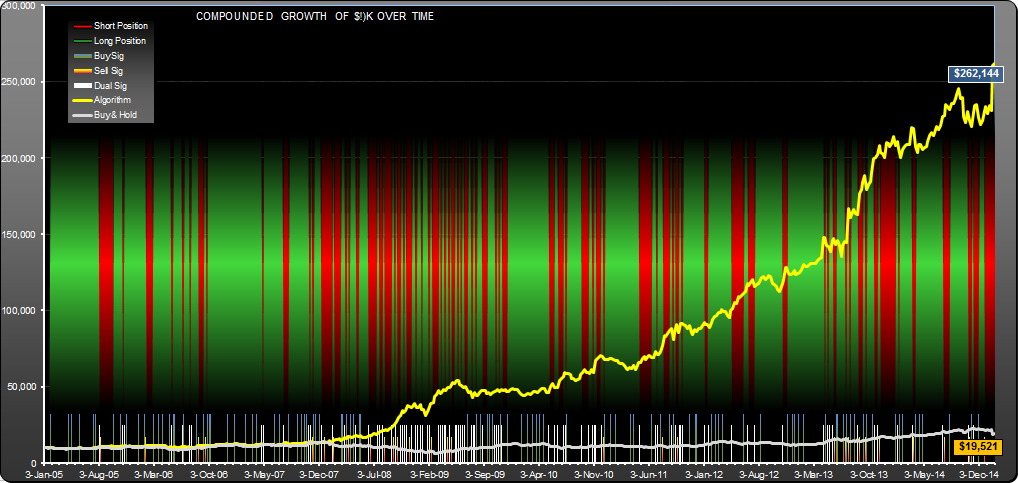

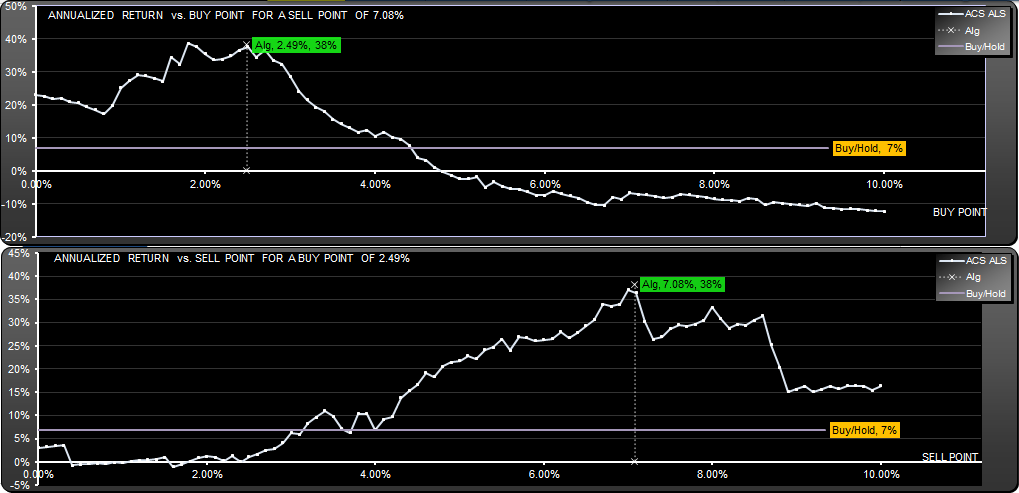

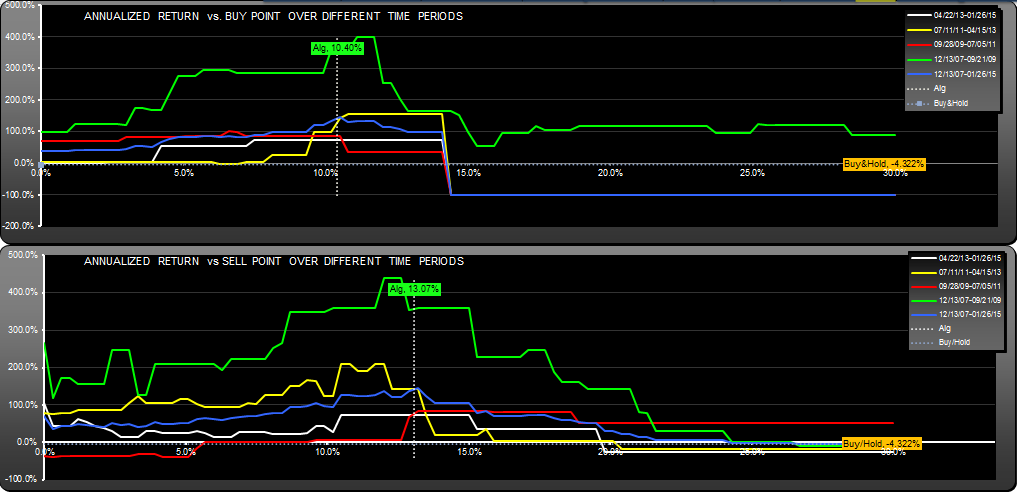

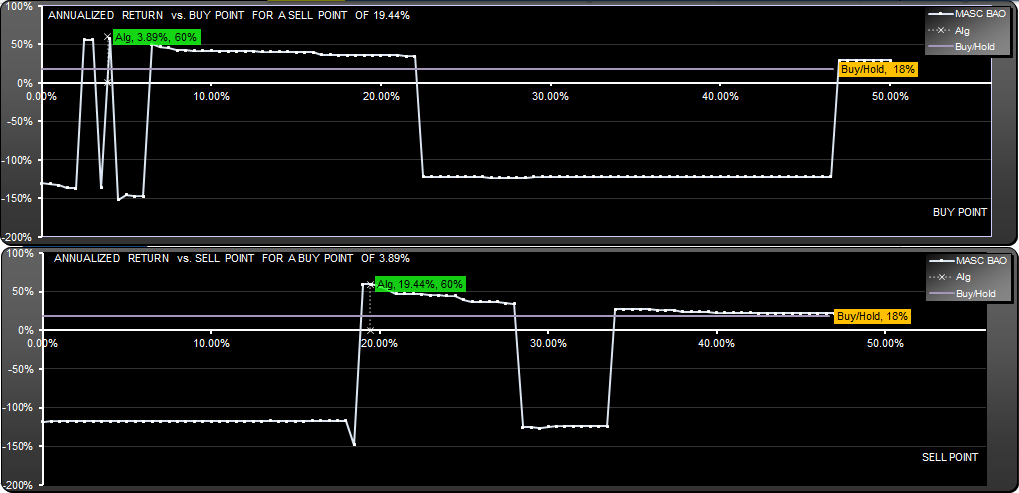

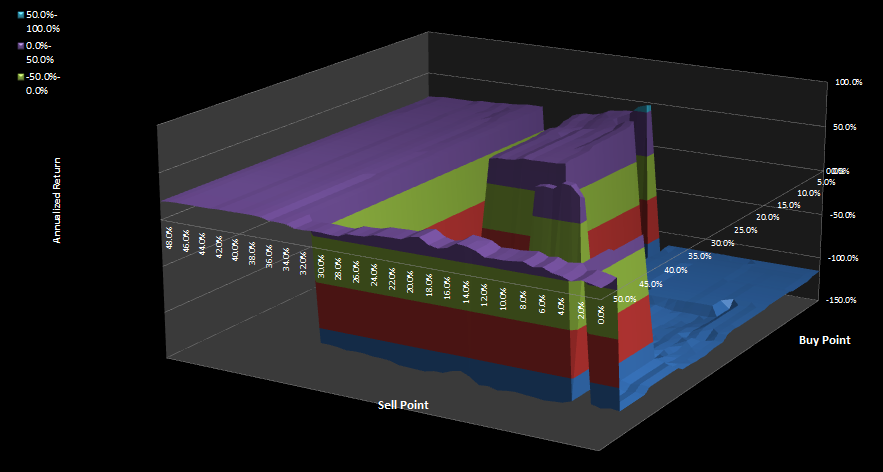

The scan shows how the return changes with choice of buy and sell point. We have chosen to show the peak, but better choices would have been in the center of the profitable regions.

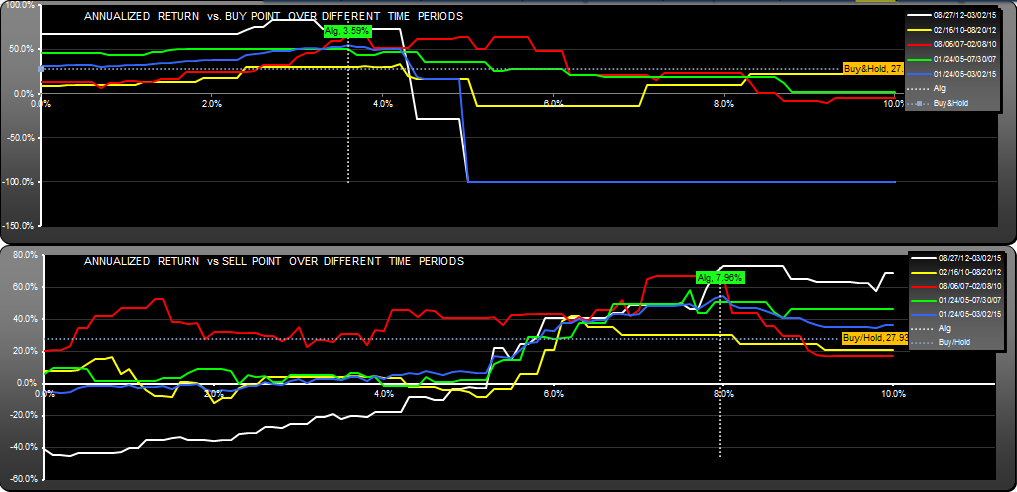

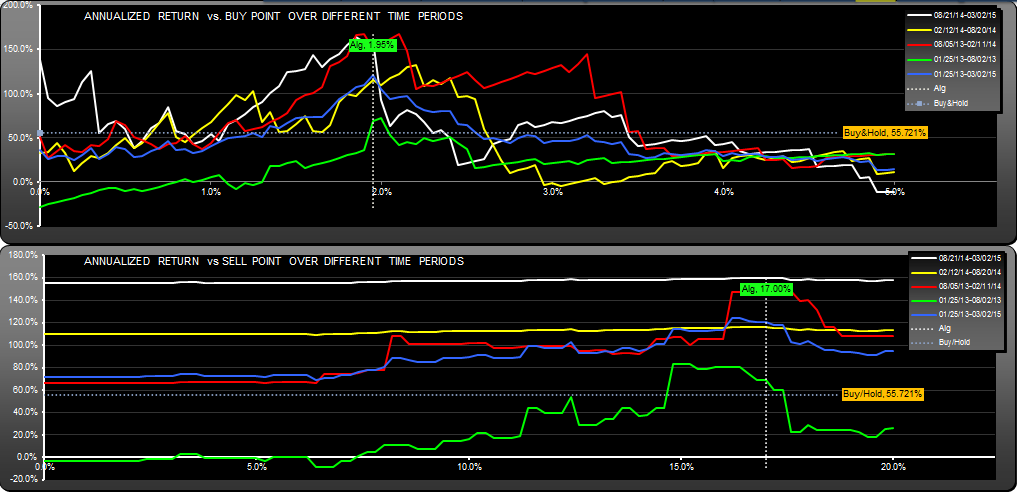

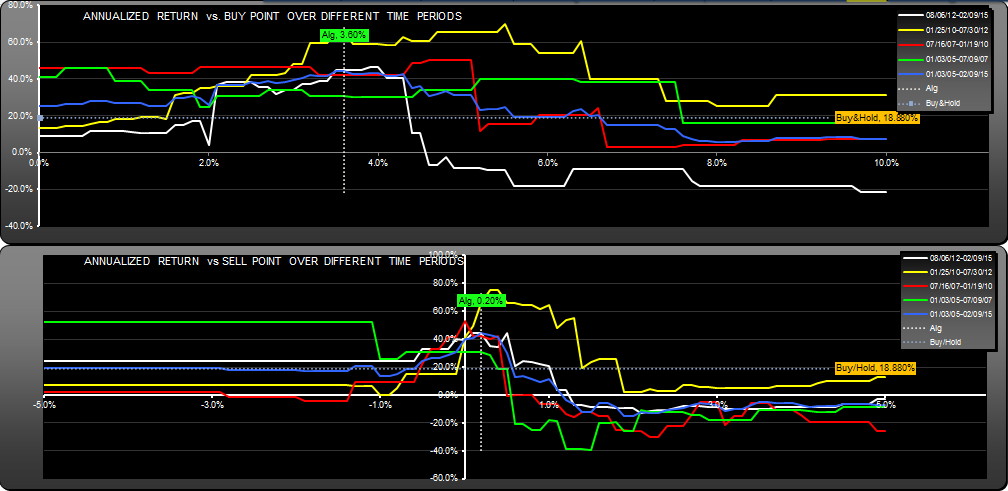

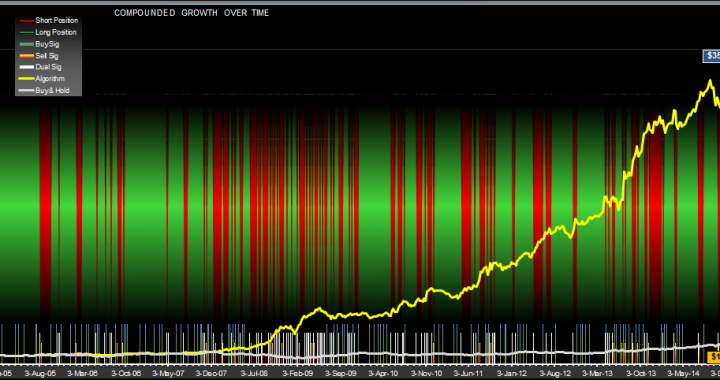

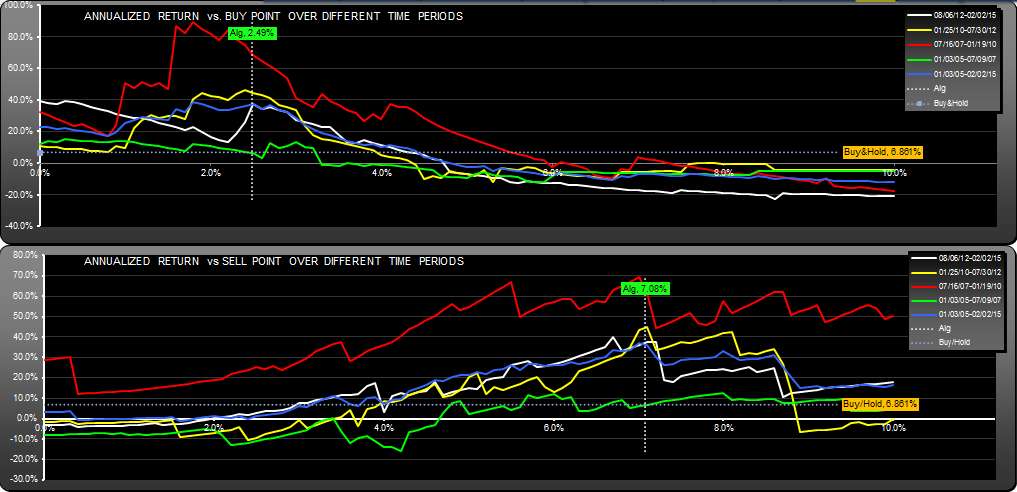

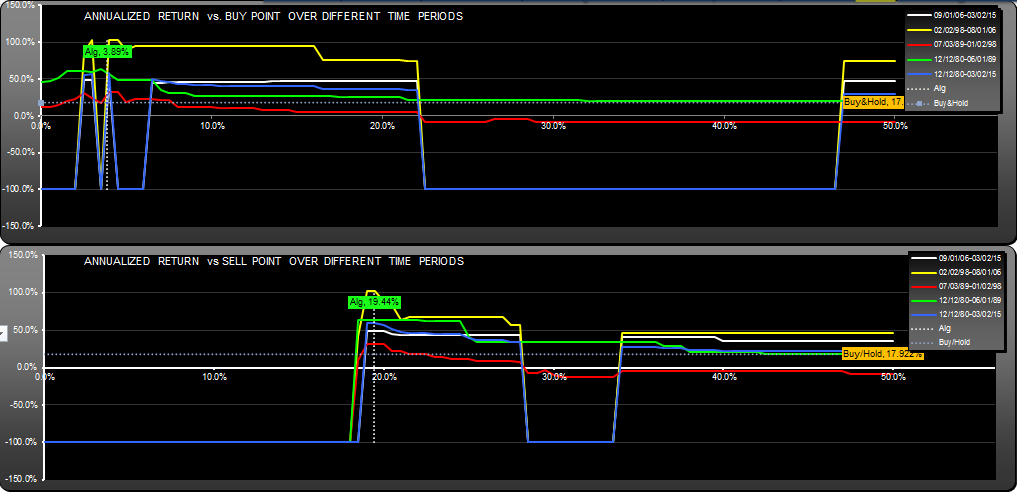

These scans show how returns change with buy/sell point for different timeframes.

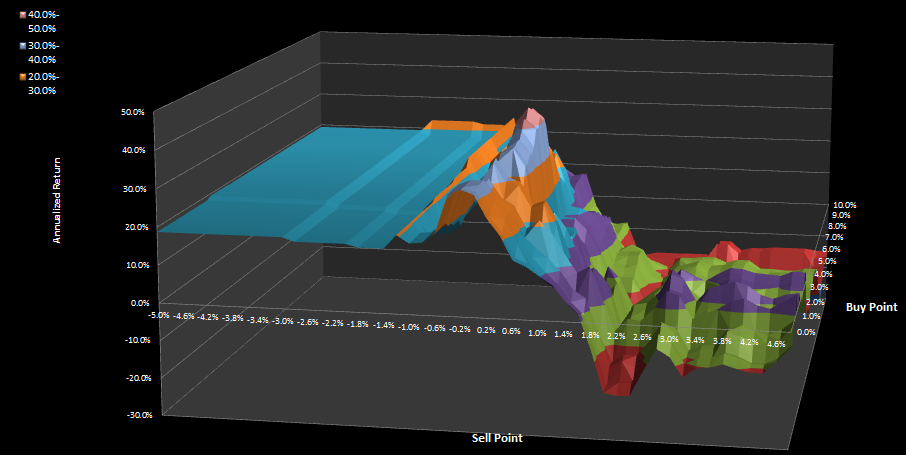

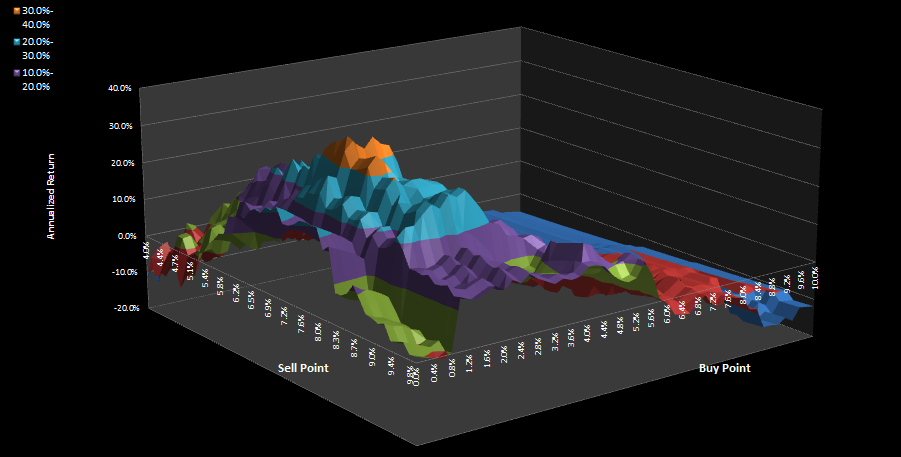

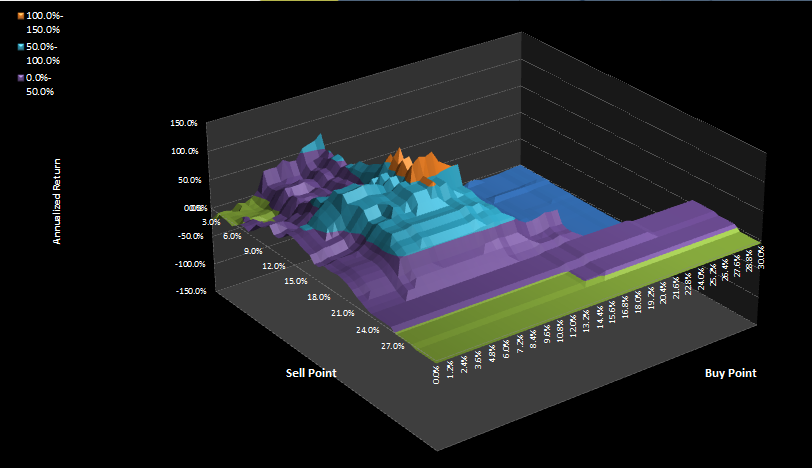

The scan shows returns for the entire buy/sell point space. High points are good, low points are, in this case, losses.

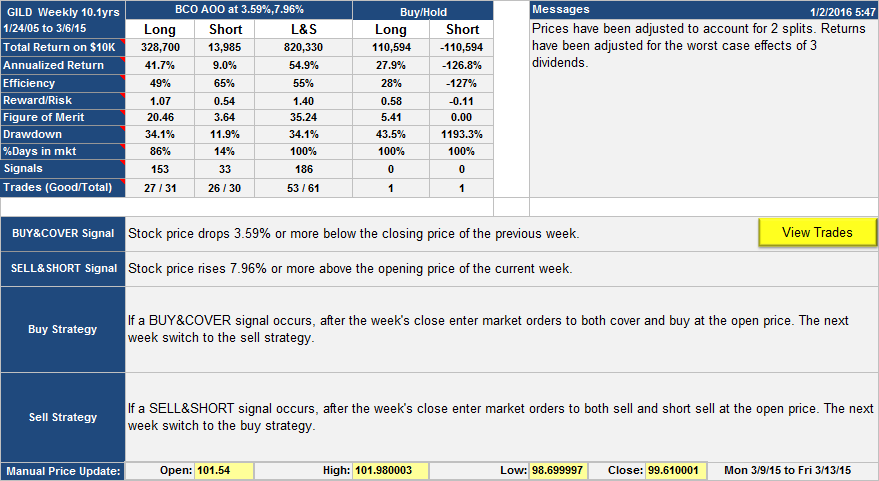

Please note that this post was edited 12/29/2105 to correct a calculation error on the short side of the algorithm.

AAPL Apple Trading Strategy (Monthly) Update 10/20/2016

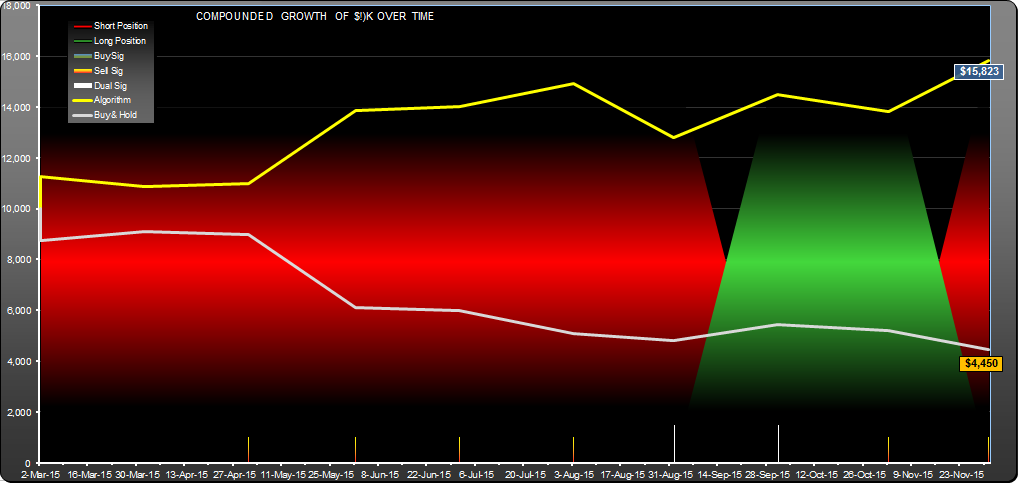

Strategy returned 11%, buy-hold -5%

AAPL Trading Strategy (M) Update 10/20/2016

AAPL Trading Strategy: Equity curve as of 10-20-2016