Methodology

Sentiment is usually based on a consensus of opinions of expert humans, however SignalSolver sentiment is the consensus opinion of multiple backtest algorithms. In the same vein as the previous few posts, this is a TECL trading strategy using SignalSolver sentiment using an adaptive threshold. For a full explanation of the SignalSolver sentiment methodology and how to interpret the simulation results, please click here.

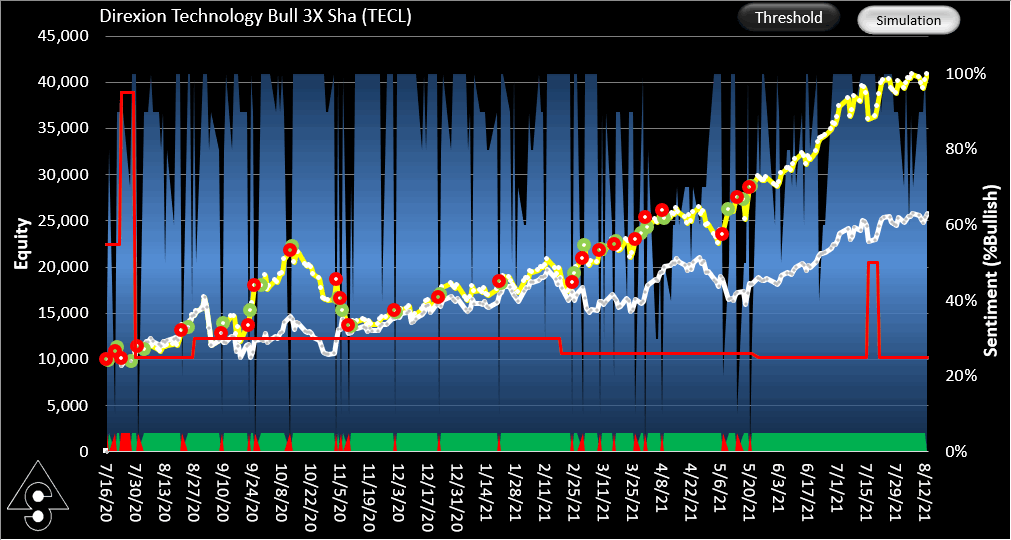

TECL Equity curve using adaptive threshold

The adaptive threshold technique examines the thresholds surface every 5 trading days (configurable) and re-optimizes the thresholds accordingly. The threshold is currently at 25% but this could change as we move forward. The buy and sell thresholds are constrained to be equal for TECL.

Performance

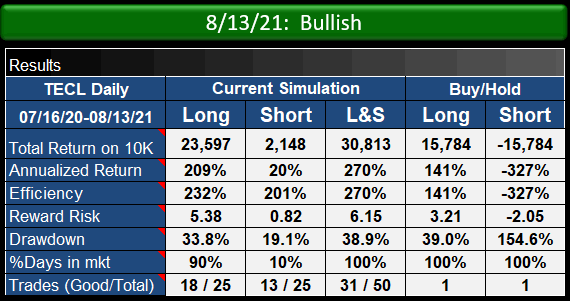

TECL trading strategy performance, using adaptive threshold

The TECL trading strategy using SignalSolver sentiment (L&S column above) has performed just under 2 times better in this simulation than buy-hold in terms of reward/risk,total return, and (CAGR). Drawdown has been around the same as for buy-hold. Just to re-iterate--this is not a backtest result, it is a walk-forward simulation using out-of-sample trading prices.

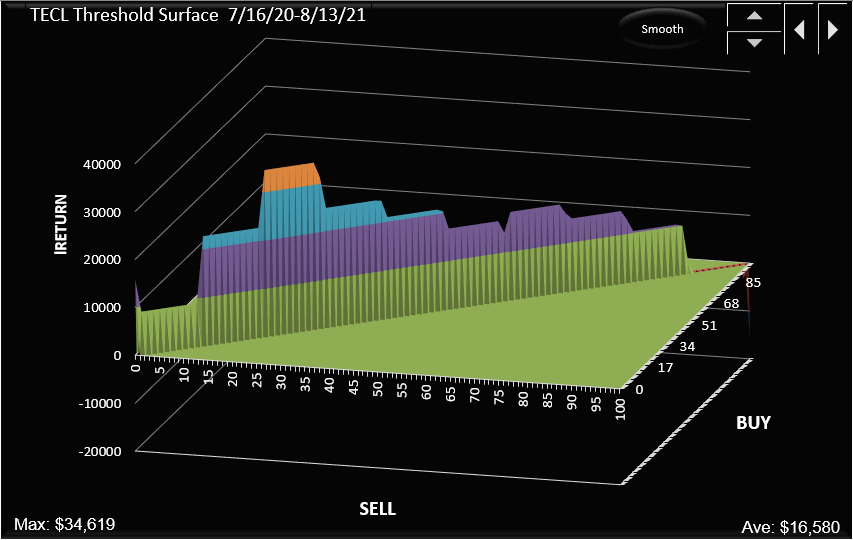

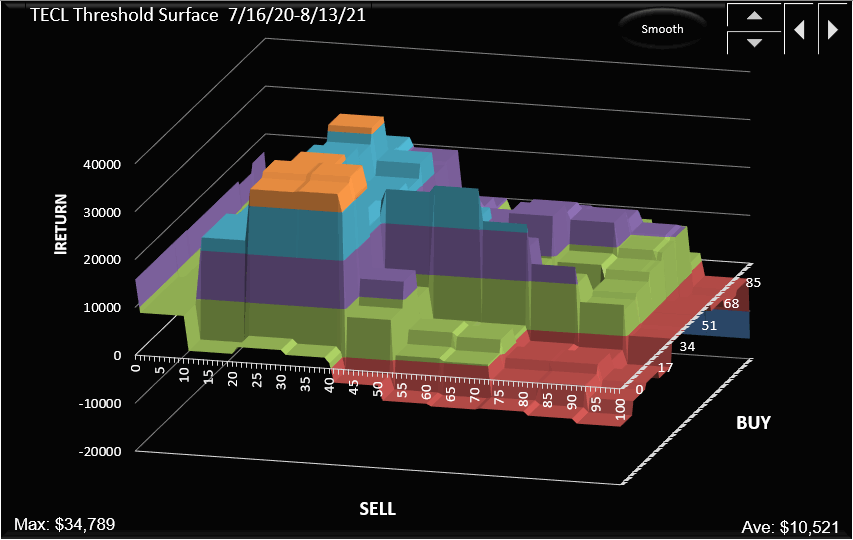

Below are the threshold surface for the entire window of 7/16/20 through 8/13/21, showing good structure both for the buy=sell constraint, and the entire surface. Note the peak is at $34,789.

Above: TECL partial threshold surface for equal buy-sell with a peak currently centered on 25%

Above: TECL entire threshold surface for the current sentiment profile

Click here to see the SignalSolver settings for this strategy: TECL Sentiment Settings

We now move into the paper-trading phase for this project. Updates will be shown below.