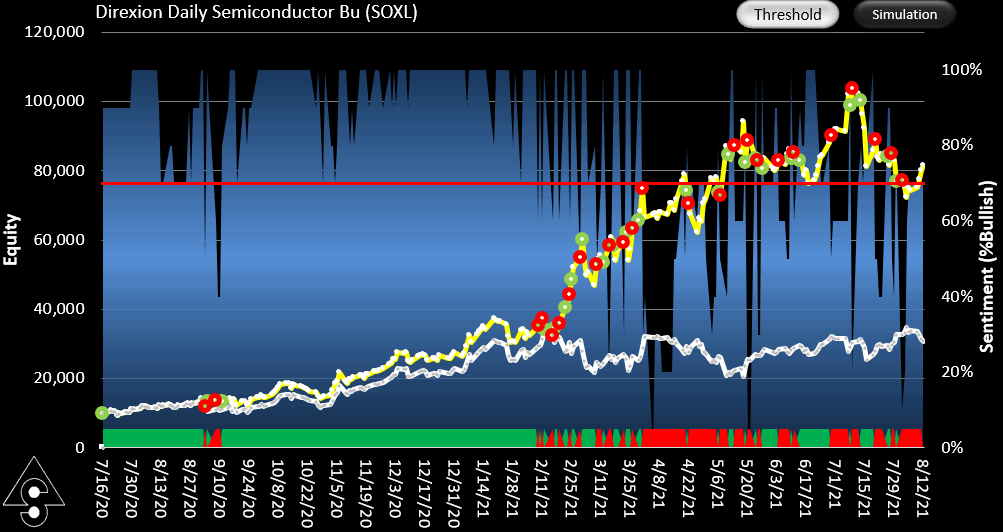

Showing the equity curve for constant threshold

Methodology

In the same vein as the previous few posts, this is another SOXL trading strategy using SignalSolver sentiment, this time we use a threshold of 70%. For a full explanation of the SignalSolver sentiment methodology and how to interpret the simulation results, please click here.

The 70% threshold showed up as the optimum mid May 2021, (below) so we will start our paper trading with that value. The constant threshold result is shown above, but this is a backtest not a walk-forward test as shown below. The equity curve is currently showing a good deal of drawdown at 21%. However let's see what happens with SOXL since it shows nice structure on the threshold surface. Is it breaking down? or will it pick up and perform well like it has in the past.

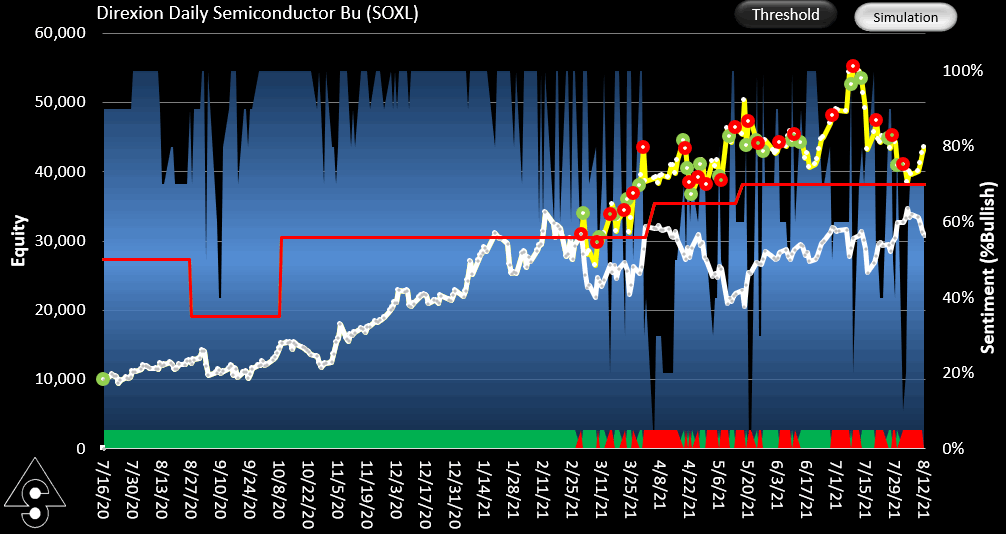

SOXL trading equity curve for simulation using adaptive thresholds

Performance

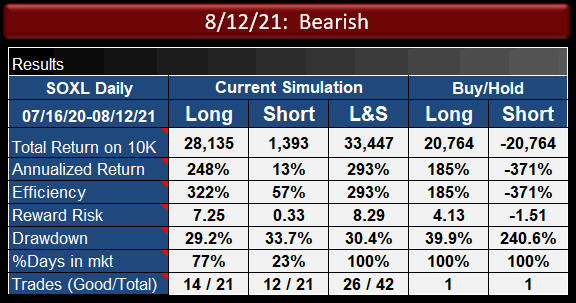

Performance of the simulation

Trading on sentiment (L&S column above) performed around 2 times better in this simulation than buy-hold in terms of reward/risk, with annualized return (CAGR) being around 1.6 times better for Long/Short trading of the signals and trading long only being, unsurprisingly, most of the gain. In all cases, drawdown was lower for the sentiment trading than for buy-hold. Its easy to forget that what you really want from a trading strategy is not necessarily to beat both long-hold and short-hold, which is quite hard to do for something with a high annualized return, but simply keeping on the right side of profitability has a lot of merit. This strategy exceeded that goal so far.

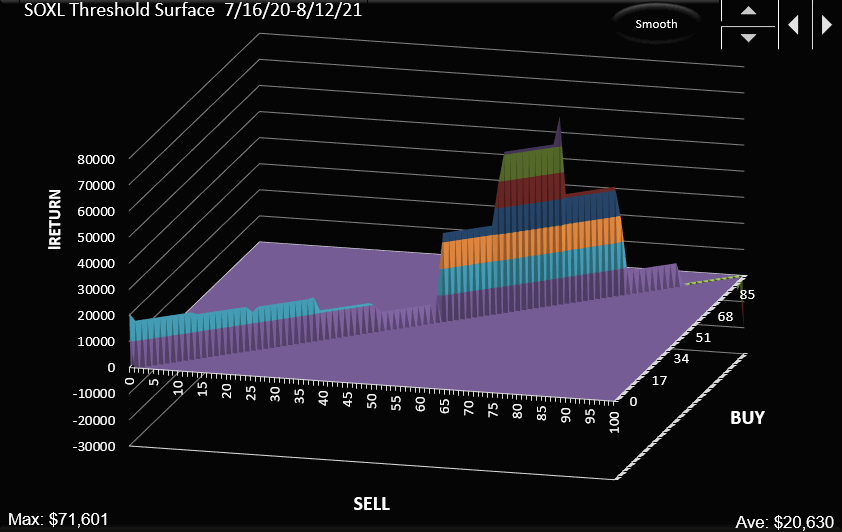

Below is the threshold surface for the entire window of 7/16/20 through 8/12/21, showing a good structure, but with somewhat of a offset. Ideally I would like to see the structure centered on 50% which would mean that the backtests are more neutral in their sentiment reading, but this may correct in the future.

Partial threshold surface for the simulation--equal buy and sell thresholds

Click here to see the SignalSolver settings for this strategy: SOXL Sentiment Settings

We now move into the paper-trading phase for this project. Updates will be shown below.

Updates

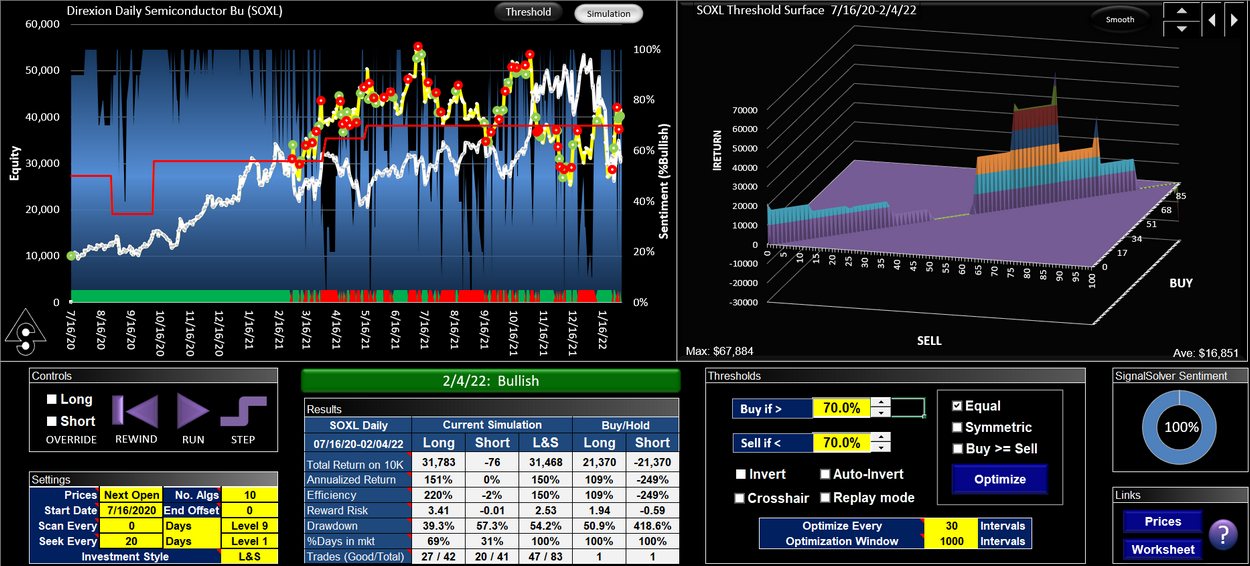

Updates to this strategy and current sentiment were reported on another page up until 4th Feb 2022 when the SOXL algorithm was reporting a 4% loss (from the go-live trading date of 16th July 2021) compared to a gain of 23% in the underlying stock. Lets look at strategies which worked better.

We have reported success with AAPL, TQQQ and FNGU in using an adaptive threshold instead of a fixed threshold. However with SOXL we were actually using an adaptive threshold to start with. Here is the dashboard as of Feb 4th 2022:

SOXL trading using SignalSolver sentiment and an adaptive threshold. The buy and sell thresholds are constrained to be equal. This turned out not to be the best choice

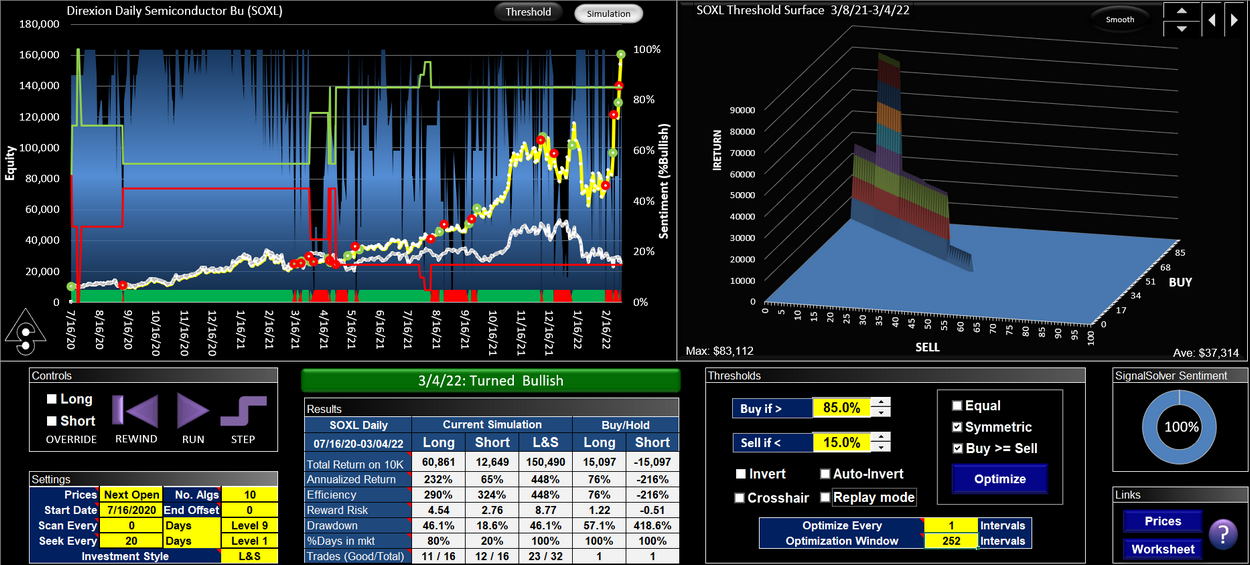

We constrain the buy and sell thresholds to be equal. We optimize the threshold every 30 trading days and use a window of 1000 trading days (effectively including all the sentiment data points every optimization). As we mentioned, this led to a 4% loss on Feb 4th. However, as of March 8th 2022, the algorithm has recovered and shown dramatically better performance than buy-hold, currently showing a 164% gain (July 16th 2021 to March 8th 2022) vs a 19% loss for buy-hold.

SOXL algorithm performance using SignalSolver Sentiment as of March 8th 2022. It has recovered from the Feb 2022 drawdown and reached new heights

Its important to know that the result you are looking at was fully reslizable. We outlined the strategy in the original post last August and if you had set up the algorithm as detailed above and followed it's signals as we walked forward, you would have made these returns.

Using Symmetrical thresholds

An even better algorithm would have been to use Symmetrical thresholds where the buy and sell thresholds sum to 100%. We optimize the thresholds every day and use a one year optimization window (252 trading day). We also apply the constraint that the buy threshold is greater than the sell threshold.

SOXL trading strategy using SignalSolver sentiment. The same sentiment plot as above, but with the adaptive thresholds set to by symmetrical.

Using these thresholds would have yielded a gain of 133% for the test period 16th July 2021 to Feb 4th 2022. As of today (3/6/2022) it is showing a 399% profit vs. a 2% loss for the underlying stock from 16th July 2021. This is the same methodology that worked well for AAPL. Here, we haven't changed the way the sentiment is generated (the Settings section is the same and the blue bar-chart is the same), we have only changed the way we handle the buying and selling thresholds for that same sentiment profile. Using freely floating adaptive thresholds (Buy threshold>=Sell threshold) gave a very similar result.

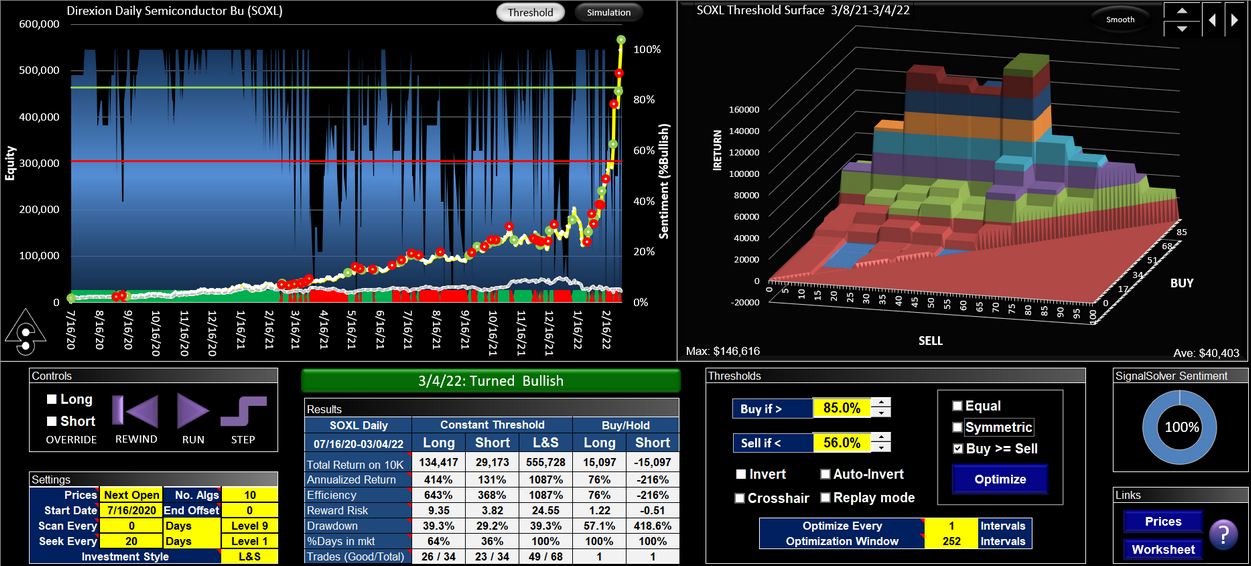

The best constant thresholds for overall gains were 85% buy and 56% sell, shown below. These thresholds were established in July 2021, but the optimum sell threshold shifted several times subsequently, so this was only realizable if you had made a lucky guess.

SOXL Sentiment trading using constant 85% buy threshold and 56% sell threshold. Sadly, there was no way to know in advance that these thresholds would have good performance.