Frequent reversals characterize this strategy for Omeros Corporation

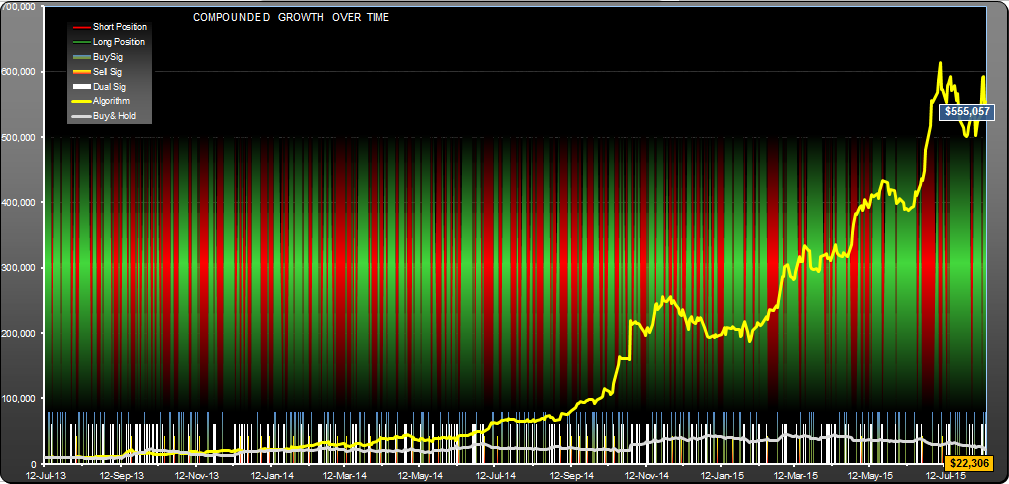

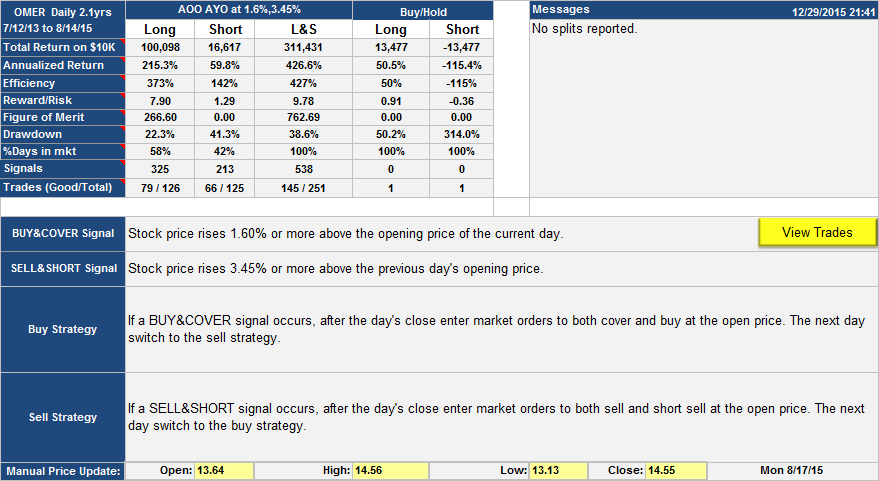

This OMER trading strategy is signal rich; there were 174 dual signal days out of the 528 days in the analysis. Added to that 151 buy signal only days and 39 sell signal only days and you get 364 signal days, of which 250 were actionable signals leading to trades, of which only 146 were good. Still, all that activity led to a theoretical $311,341 profit from $10K invested over the 2 year period from 7/12/13 to 8/14/15.

The algorithm itself is a bit of an odd one with buys triggering off price changes from the open price and sells triggering off price changes from the previous day’s open price. Is it just a fluke that it has worked so consistently? In its worst quartus (132 trading days in this case) this algorithm returned 250% annualized or 93% actual return.

You can see from the list of trades and the equity chart that there were several periods of daily reversals from long to short and back again. You might think that ignoring dual signals would work better, but it doesn’t–it leads to an 80% reduction in returns.

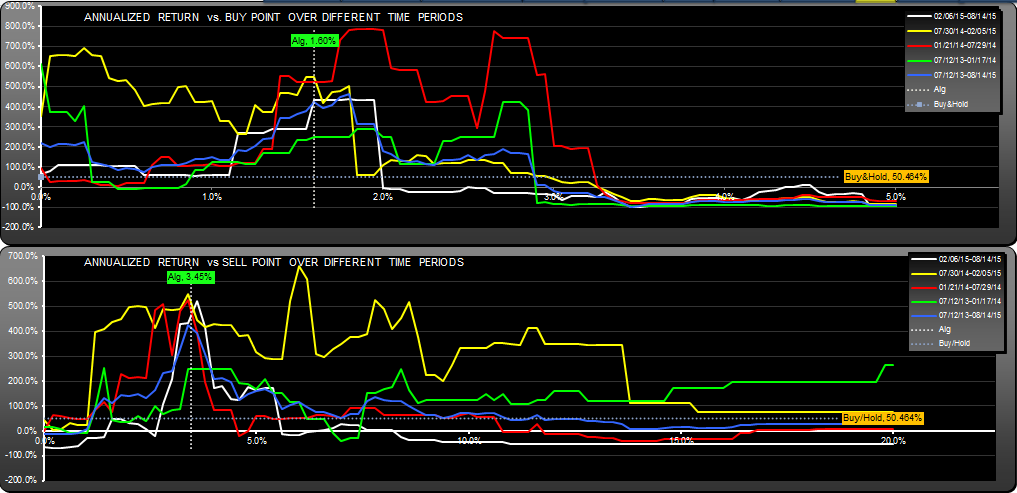

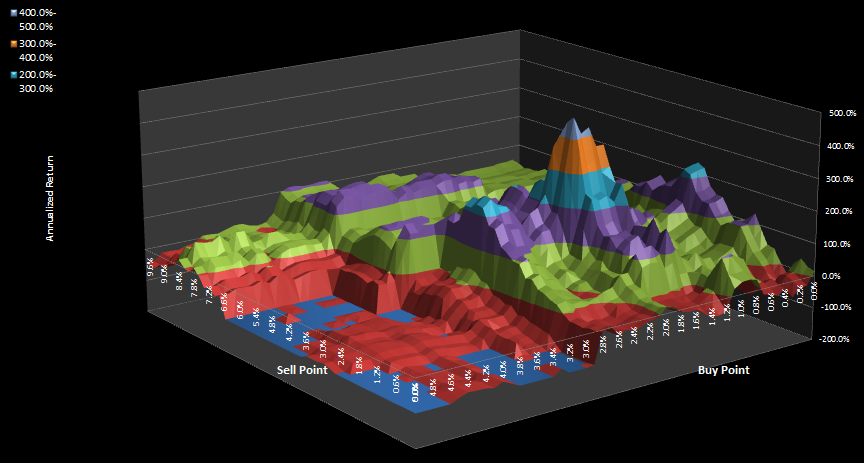

This strategy was found by optimizing for minimum quartus returns and then doing some minor tweaking by hand, which is quite easy to do since the Scan charts in Signalsolver are interactive. I just moved the buy and sell points to areas away where there were lower returns. I’m just going to post the charts, if you need help interpreting them I would refer you to yesterday’s AAPL post where I discuss the methodology in detail.

By the way, OMER took off today gapping up 70% or so. I was working on it before that so this change doesn’t show on the data, but the proceeds would have jumped to $929,212. It would be cheating to track this strategy knowing it had already added 70%, so I’m not planning on doing so.

Andrew

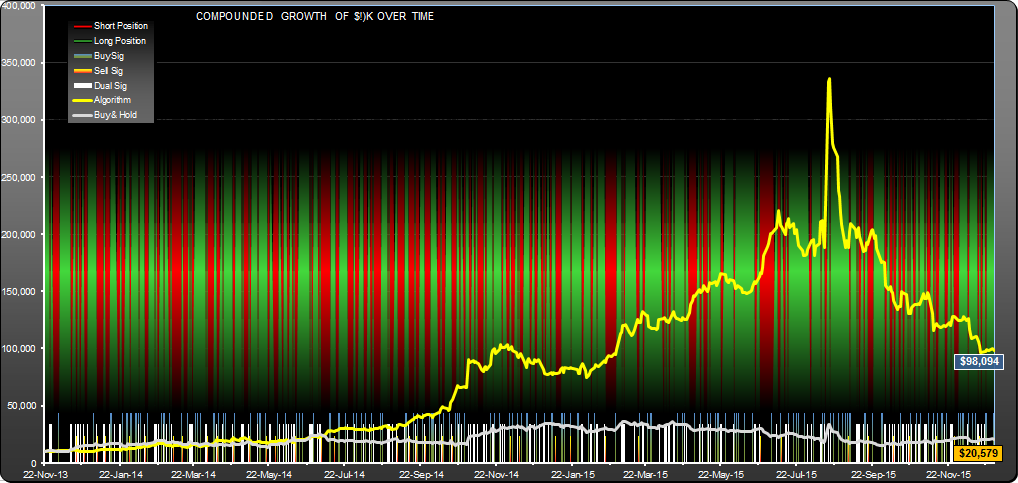

Equity curve for the OMER trading strategy showing $545,057 in returns over a 2 year period.

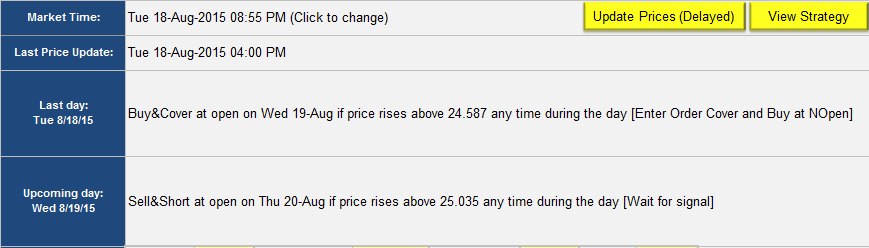

OMER Daily algorithm–current and pending trades, if you are looking for synchronization info.

Follow up 12/29/2015

This algorithm peaked and then failed dramatically immediately after the 70% gap up on Aug 18th, very shortly after publication. Here is the 528 day equity curve:

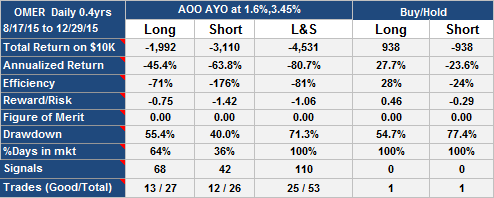

Here are the stats:

Buy-hold would have been a much better option. For a profit, one solution was a buy point of 2.0% and a sell point of 4.4%, which would have given a return of $13,964 over the 94 days. Unfortunately, these parameter changes don’t appear to be predictable.

Andrew