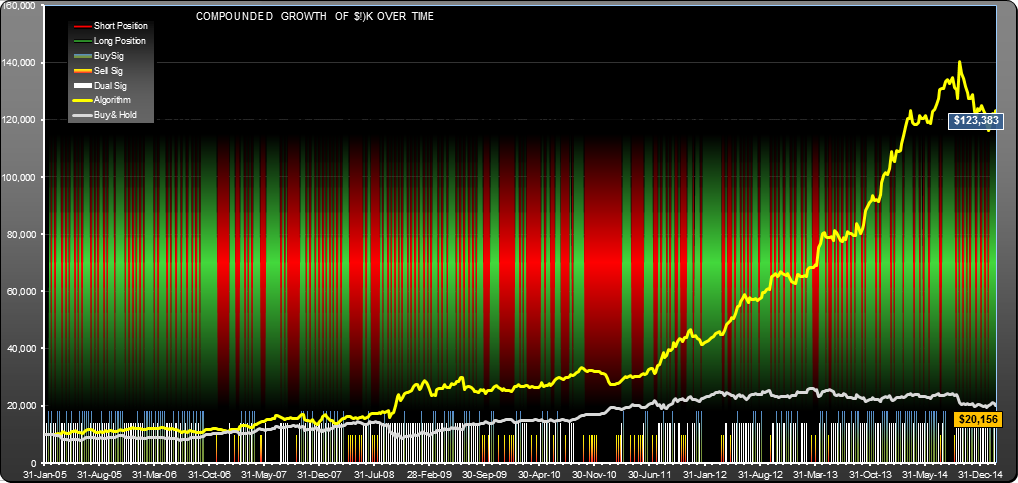

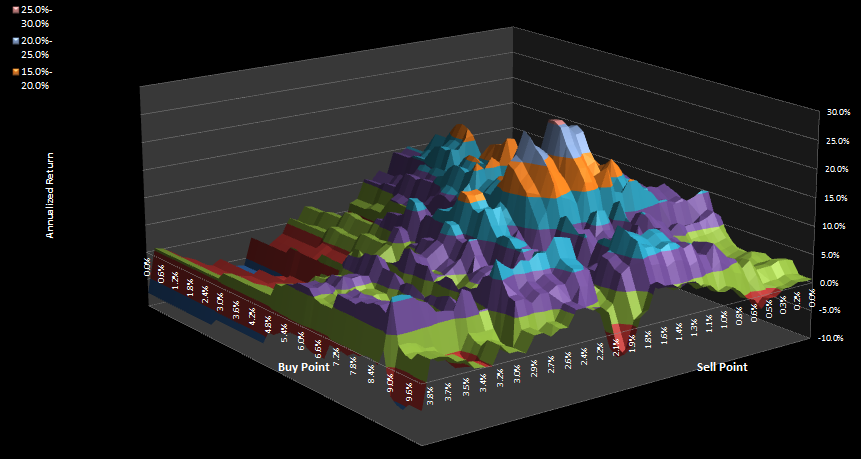

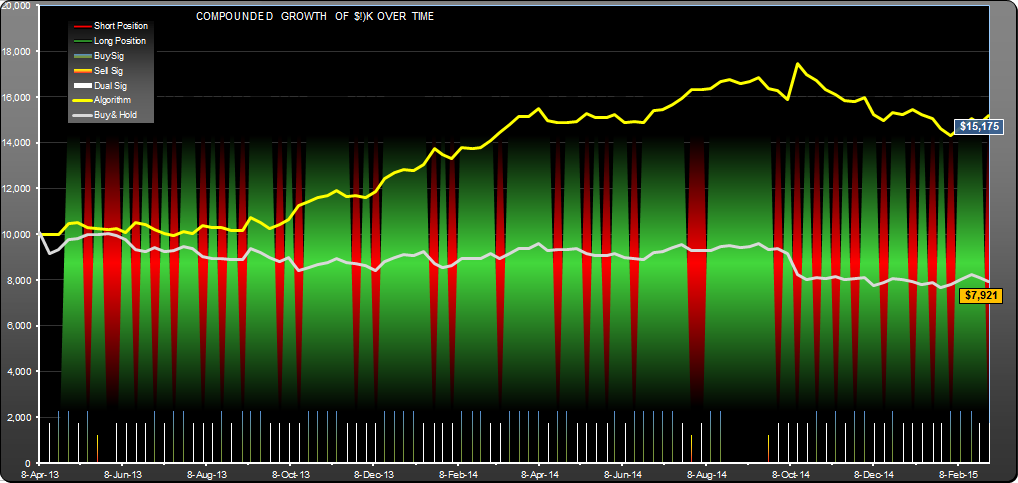

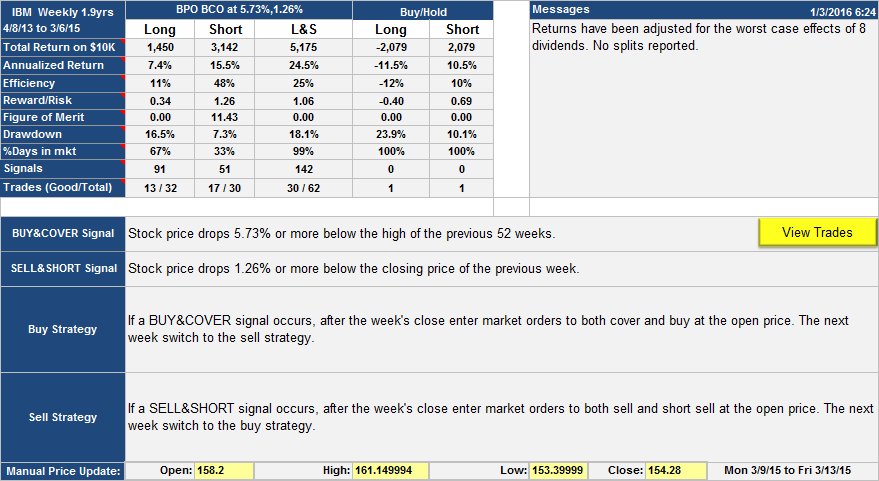

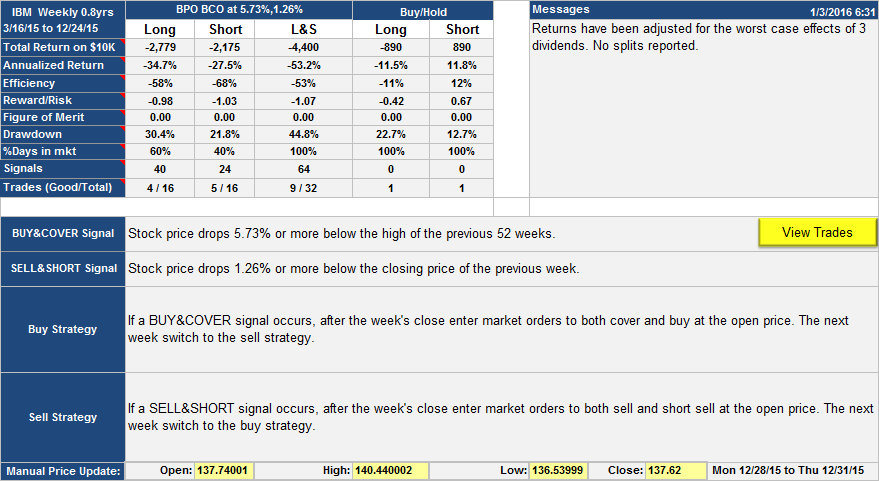

This IBM trading strategy made 11x the total returns (4x the annualized return) of the underlying stock with half the drawdown. The backtest period was 10years. The strategy itself (see table below) was straightforward with both buy and sell signals triggered by falling prices. The buy signal keyed off the 52 week high while the sell signal keyed off the closing price of the previous week. All buying and selling was done at the weekly open. It turns out that 225 out of 528 weeks were dual signal days, this often led to periods where a buy weeks alternated with sell weeks (see list of trades in excel format). Ignoring dual signal days would have led to very low gains, so the alternating strategy must have worked somehow.

The strategy had a buy bias, there were 141 days with just a buy signal and 55 days with just a sell signal. Since the underlying stock seems to be downwardly trending, this bias may work negatively if the downtrend continues. We shall see.

The backtest assumes a commission of $7 per trade.

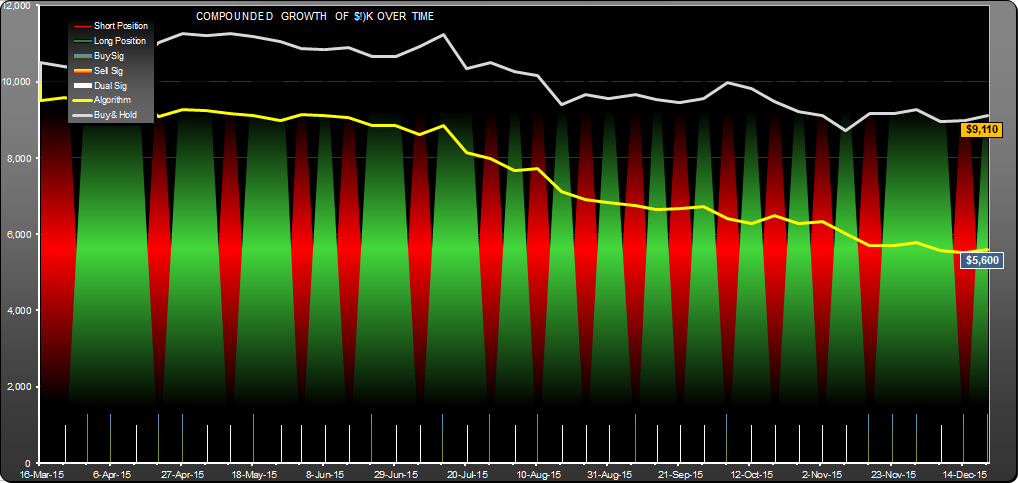

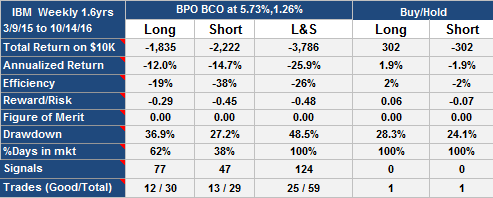

Update, 5/26/2015

Since publication on 3/16/2015, the strategy has decreased -1.04% (-5.3% annualized) while the underlying stock has increased 9.68%. There were 7 trades, 4 successful, 10 buy signals and 4 sell signals.

Andrew