Please note, this post was corrected 1-3-16 to account for a short-side error in the original calculations. Apologies for this.

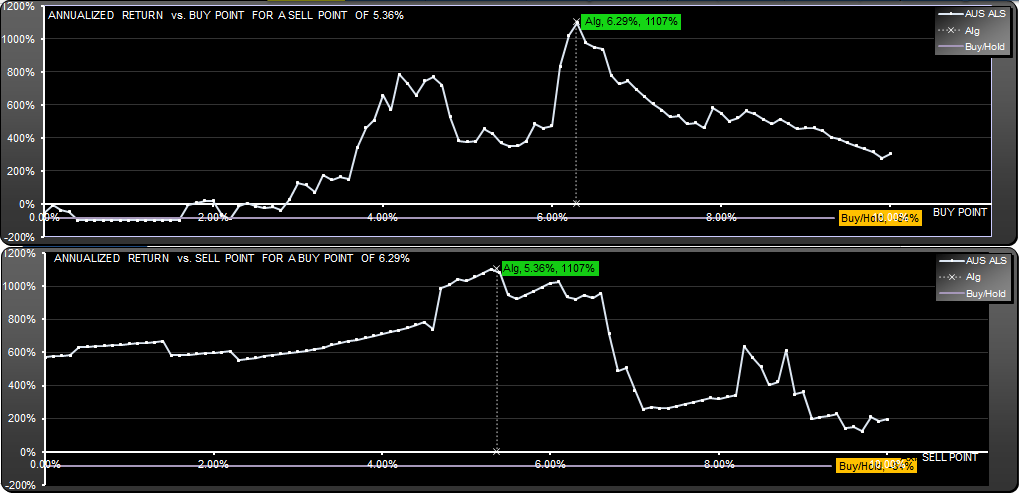

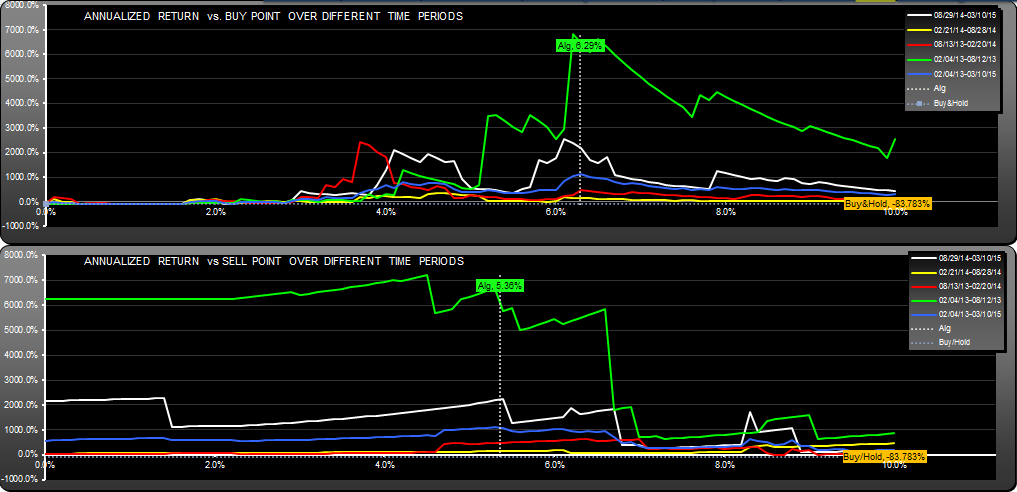

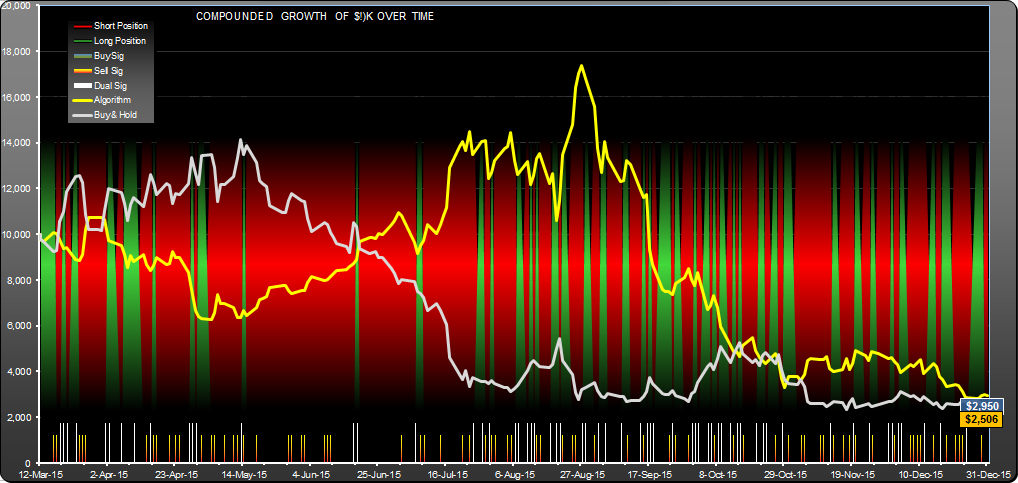

This NUGT trading strategy (Direxion Daily Gold Miners Bull 3X ETF) gave a theoretical $1.8 million profit for a $10K initial investment over 2.1 years. The trading strategy required once a day attention. Signals were triggered by rising prices on both the buy and sell side. The buy side reference was 1.0629 times the average of the previous day high, the previous day low and the current day open. You would need to calculate it every day after the open and then put in the buy and cover orders, if you were short. On a few occasions this meant buying at the open price, but usually there was time to get the stop orders in.

The sell side target was a bit simpler, 1.0536 times the previous days low. You could enter the sell and short limit orders after each close, if you were long.

There is a Bear version of this fund, the Direxion Daily Gold Miners Bear 3X ETF (DUST), however the results would have been different if you had used it for the short side.

Here is the list of trades.

Hello,

I’m interested in your NUGT Trading Strategy (Daily). How do I access it?

Thanks!

Bryan

Hi Bryan,

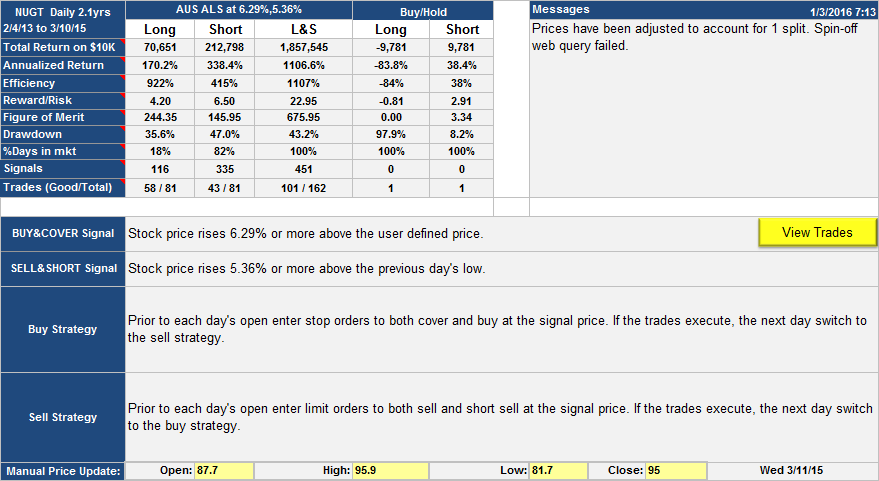

I’m glad you find it interesting. The entire strategy is detailed in the table above. On March 12 the strategy went short, so March 13 would be buy strategy day. The user defined price is the Mar 12 high (9.84) plus the Mar 12 low (9.00) plus the March 13 open all divided by three. Multiply that by 1.0629 to get the March 13th target buy price, You can get more insight by studying the list of trades, the link is above.

Please note that the strategies published here are for education and discussion purposes only.

Regards,

Andrew

Update 5/26/2015:

Since initial publication on 3/12/2015, this strategy has lost 28.82% (-82.2% annualized). The underlying stock, NUGT, has increased by 31.58% (+302% annualized). There were 47 signals and 19 trades, 8 profitable. The algorithm peaked on 3/11/2015 then fell into a trough on 5/4 with a drawdown of around 40.8%.

Andrew

Hi Dr. MacLean, I emailed you yesterday…not sure if you got it. I just remembered that I might have actually sent it from the signal solver page.

Anyways, thanks a lot for such an informative site…I’ll sign up for your subscription. I was looking at the nugt strategy…you mentioned that “..the user defined price is the Mar 12 high (9.84) plus the Mar 12 low (9.00) plus the March 13 open all divided by three. Multiply that by 1.0629 to get the March 13th target buy price”. Can the formula be tweaked to see how it performs without taking the opening price of the same day? That would be March 13th data in the above example you shared.

Would love to hear from you….thanks in advance.

Andrew,

can you clarify what is meant with regard to “Signals were triggered by rising prices on both the buy and sell side.”? I am trying to reverse engineer the spreadsheet but i’m not sure what triggered you to take a trade?

The signals were generated by rising prices. See the table above with the Signals and Strategies. No need to reverse engineer anything, this strategy has stopped working.

Andrew

Dear Andrew

With grate interest I studied your NUGT and DUST strategies. Could you provide me with more inside information, such as the formulas, so I can run a back test my self?

Thank you very much.

Hi Thomas. Both strategies are fully detailed in the posts, I believe. Please refer to the Signals and Strategy section of the screenshots. The only other thing you need to know is that the user defined price is the daily (H+L+O)/3. I’m rather surprised you are interested in this NUGT strategy since it stopped working in August 2015 (see Jan 16th update). Since then, the losses have been close to 90%. After original publication there was a decline, then for 3 months or so it worked quite well before failing. As I have said before, you can easily find good backtests with SignalSolver, but the strategies you find don’t usually last for long.

Andrew