These TQQQ signals (weekly) traded as directed would have performed around 20.8 times better than buy-hold with an ROI of 85,602% for the period 08-Feb-10 to 14-Sep-18

TQQQ signals (weekly) shown above were chosen for their reward/risk and parameter sensitivity characteristics. Backtests don't always generate reliable signals which can be counted on moving forward but many traders find value in knowing what buy and sell signals would have worked well in the past.

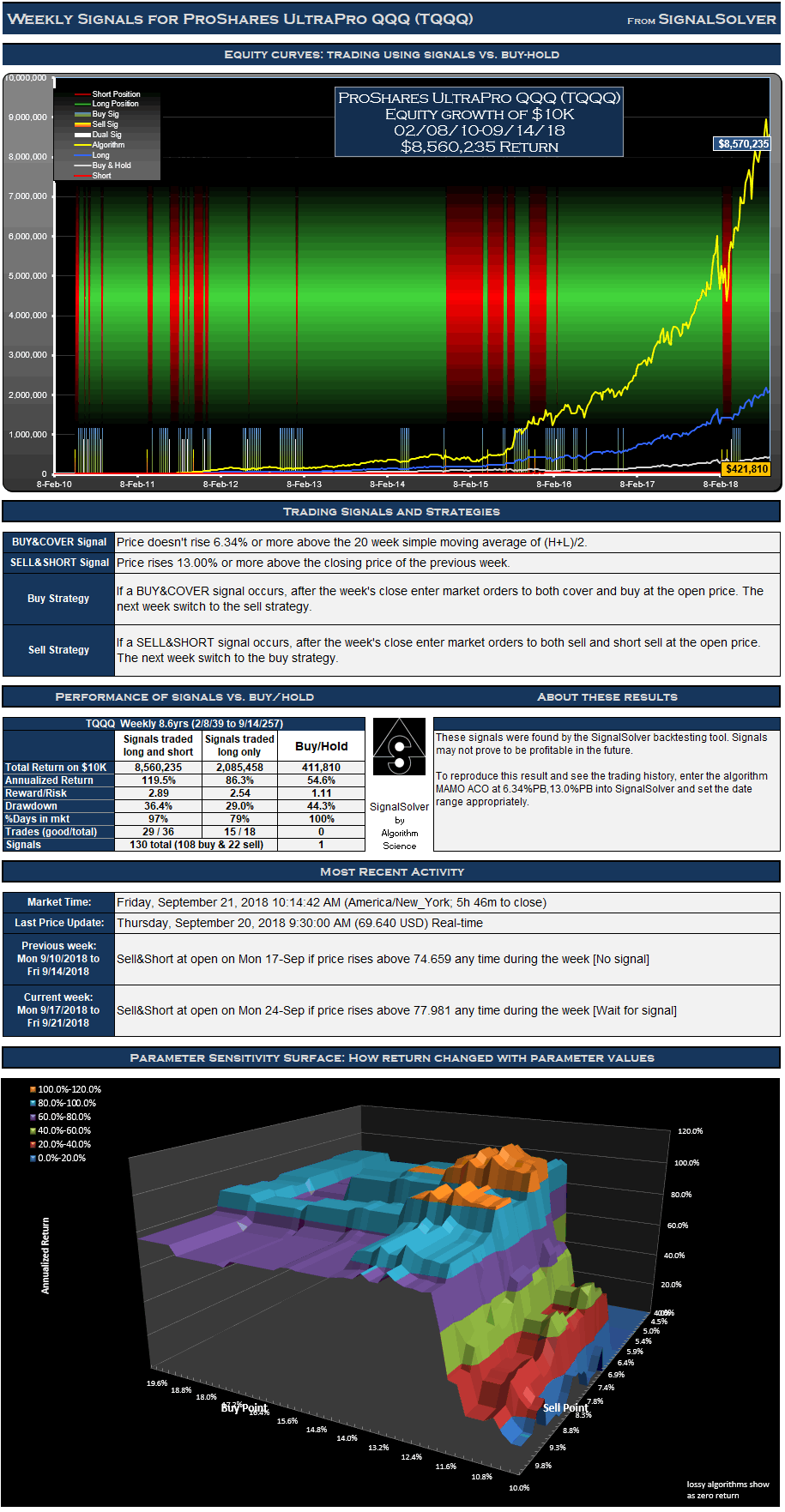

Returns for the TQQQ signals

For the 449 week (8.6 year) period from Feb 8 2010 to Sep 14 2018, these signals for TQQQ traded both long and short would have yielded $8,560,235 in profits from a $10,000 initial investment, an annualized return of 119.5%. Traded long only (no short selling) the signals would have returned $2,085,458, an annualized return of 86.3%. 78.7% of time was spent holding stock long. The return would have been $411,810 (an annualized return of 54.6%) if you had bought and held the stock for the same period.

Signals and Trades

Not all signals are acted upon and signals are often reinforced in this type of strategy. If you are long in the security, buy signals are not acted on, for example. Similarly if you are short you must ignore sell signals. There were 108 buy signals and 22 sell signals for this particular TQQQ strategy .These led to 18 round trip long trades of which 15 were profitable, and 18 short trades of which 14 were profitable. This is a weekly strategy; weekly OHLC data is used to derive all signals and there is at most one buy and sell signal and one trade per week.

Drawdown and Reward/Risk

Drawdown (the worst case loss for an single entry and exit into the strategy) was 36% for long-short and 29% for long only. This compares to 44% for buy-hold. The reward/risk for the trading long and short was 2.89 compared to 1.11 for buy-hold, a factor of 2.6 improvement. If traded long only, the reward/risk was 2.54. We use drawdown plus 5% as our risk metric, and annualized return as the reward metric.

The backtests assume a commission per trade of $7.