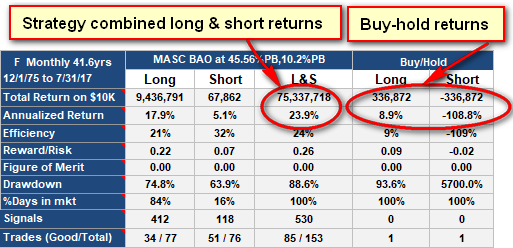

MASC BAO roughly follows a "buy the dips but sell at the first sign of trouble" methodology. The MASC BAO strategy for the Percentage Band is this:

- A BUY signal occurs if, in a given period, the price fails to rise a fixed percentage above the last sale price.

- A SELL signal occurs if the price goes below a fixed percentage below the median price (i.e. half H+L) of the previous period.

- A sell signal turns a bullish position to bearish at the open of the subsequent period.

- A buy signal switches a bearish position bullish at the close of the period.

- You only respond to one signal per time period.

For example, if the last sale price was 100, a buy signal for [MASC 10% PB] would occur if the price in a given day, week or month failed to go above 110. This could be dangerous if you were trading short or long and short. If you were short and the price broke out to new highs, there would be no buy (cover) signals and you would lose all if the price went to double your short sale price. If you were just trading long, you would be simply be locked out of a bull run.

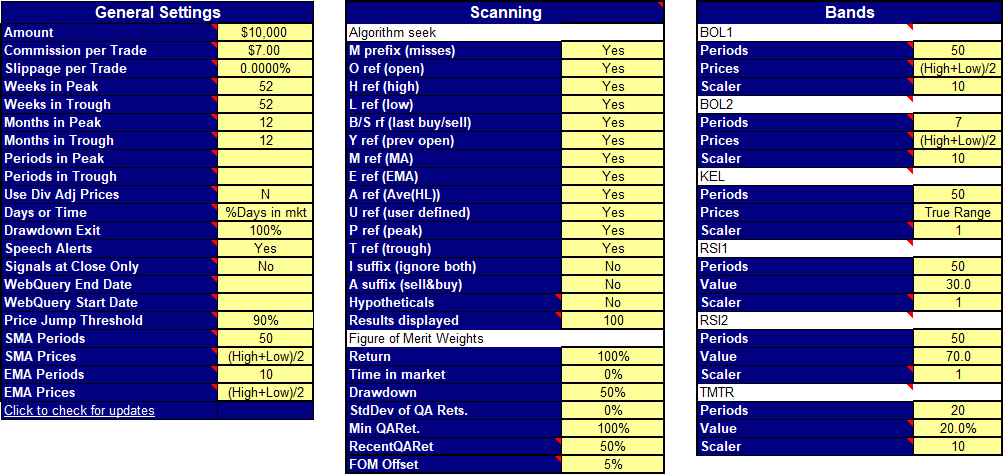

For other bands, the percentage value is calculated on the band in use and added into the reference (in this case last sale price on buys, median price on sells), as described here. Interestingly, only 4 bands emerged from this study: SMA (Simple moving average), TMTR (Trimmed mean of the true range), Bol1 (Bollinger band 1) and the PB (percentage band). Other bands often gave good results, but these four bands gave the best results.

As always, good backtest results don't necessarily translate into future profits for any trading strategy.

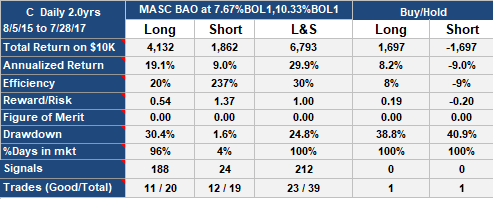

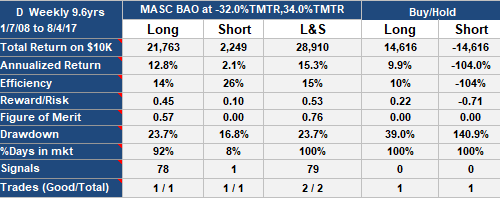

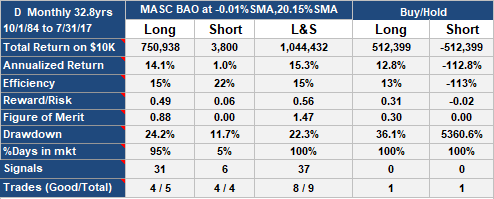

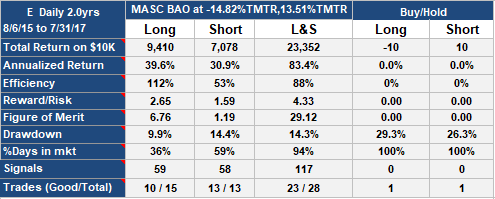

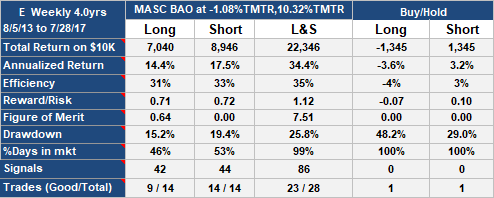

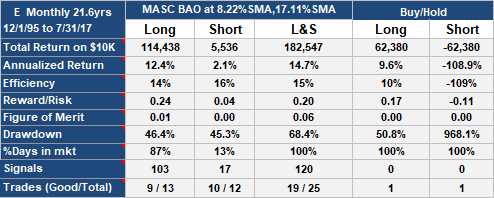

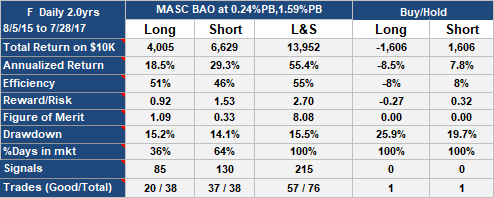

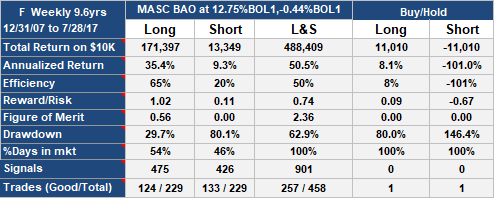

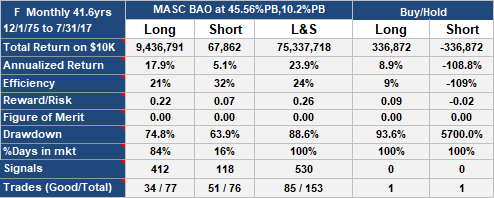

, daily data") MASC BAO Trading Strategy on A (Agilent Technologies), daily data

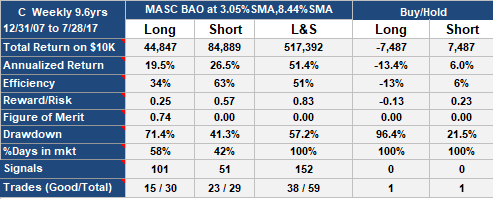

MASC BAO Trading Strategy on A (Agilent Technologies), daily data, weekly data")

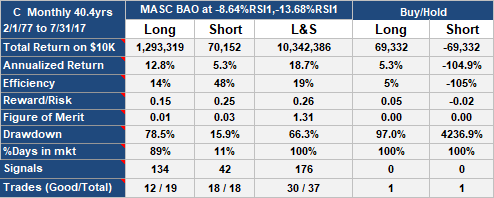

, monthly data")

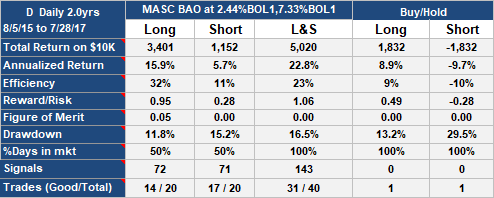

, daily data")

, weekly data")

, monthly data")

Signal Solver was working great when I first downloaded it. Today there is a popup that says: “I’m, sorry. There was an error in the back test”. Is this a known recent issue?

Tried to download again but same issue.

Hi Joseph,

Yes, sorry about that. One of the Yahoo queries (the one which fetches the latest prices) just stopped working. If the condition persists, I hope to have a workaround in the next few days.

Andrew

Thank you for the quick response. The Solver is pretty awesome.

Joseph,

I have fixed SignalSolver, it should work fine again now.

Andrew Nov 7th 2017