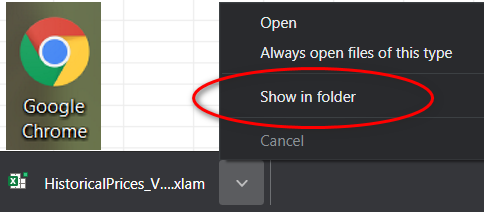

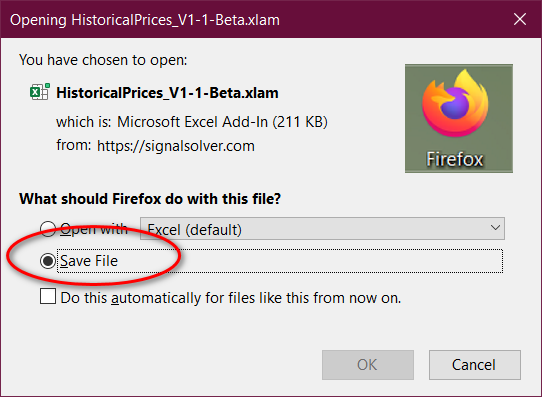

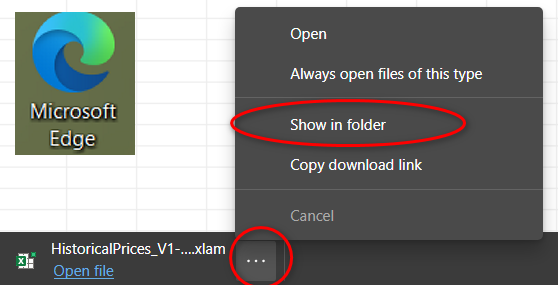

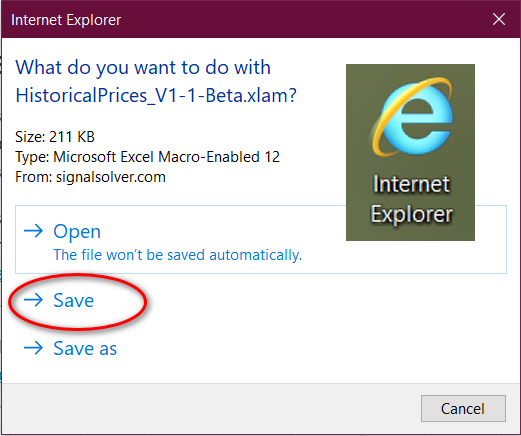

Fig1: Unblock the file by selecting the filename and right clicking, then select Properties. Under "General" properties check the Unblock box.

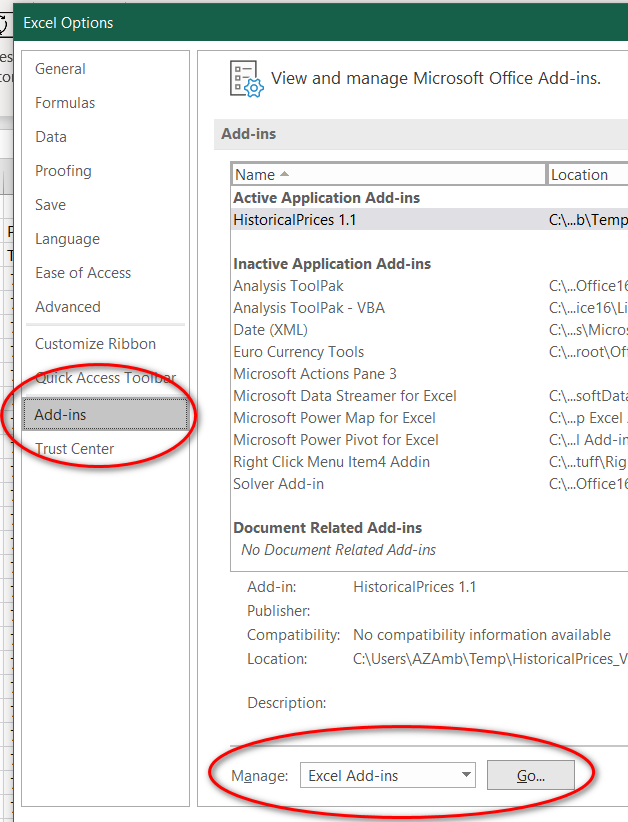

Fig.2: From the File->Options->Add-ins menu select Manage Excel Add-ins

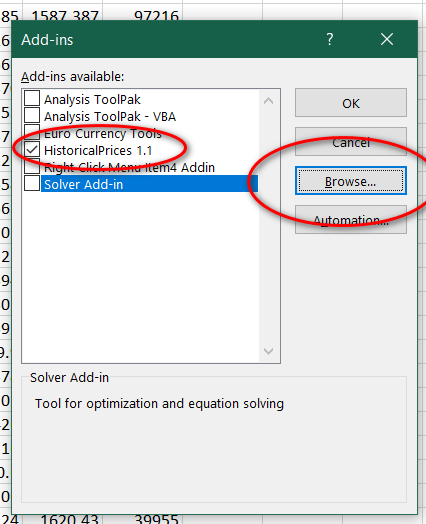

Fig 3: Click on Browse, select the downloaded .xlam file and click OK. HistoricalPrices should appear in the list as checked.

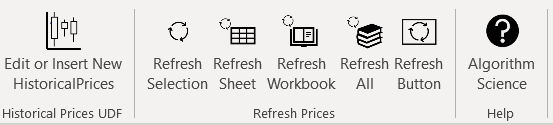

The HistoricalPrices Add-in sub-Menu

Edit or Insert New HistoricalPrices

Refresh Buttons

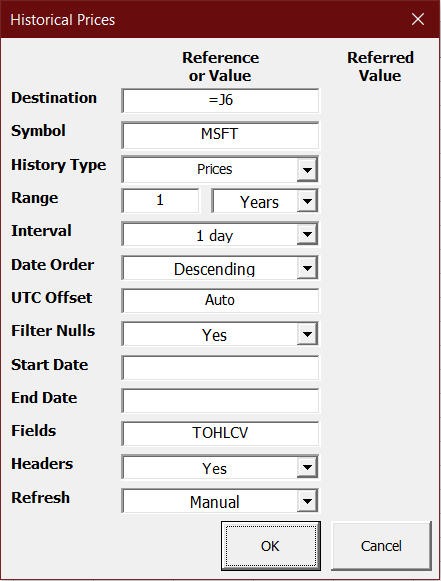

HistoricalPrices Dialog

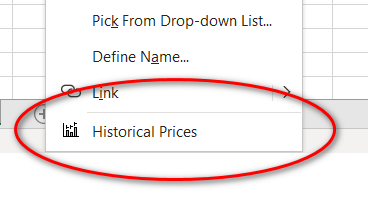

This dialog can be activated either by selecting "Edit or Instert New Historical Prices" on the HistoricalPrices menu on the ribbon, or by right clicking when a cell is selected on the spreadsheet and selecting "Historical Prices" from the context menu.

When the dialog is filled out and the OK button is clicked, a User Defined Function (UDF) will be inserted into the selected cell, or the existing UDF edited and replaced. For example, for the above dialog the UDF would look something like this:-

When the dialog is filled out and the OK button is clicked, a User Defined Function (UDF) will be inserted into the selected cell, or the existing UDF edited and replaced. For example, for the above dialog the UDF would look something like this:-

=@PriceHistory(H5,"MSFT","Prices",1,"Years","1 day","Descending","Auto","Yes",,,"TOHLCV","Yes","Manual")

The "@" sign may not be present, depending on your version of Excel. The UDF can be edited either manually or (recommended) via the dialog.

Destination

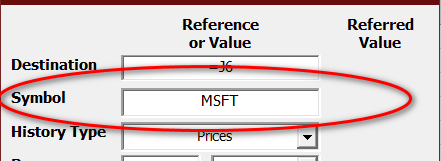

Symbol

Enter the Yahoo Symbol for the security which you wish to retreive historical prices for. You can enter a symbol or you can enter a cell reference, or just click on the cell that holds the symbol.

About Stock Symbols

You can enter any stock symbol recognized by Yahoo Finance, the spreadsheet will then fetch all the historic price data needed for analysis. If the symbol is not listed on the NYSE, NASDAQ or AMEX exchanges, you should follow the symbol with a dot, then the exchange code.

Examples of Symbols of different types

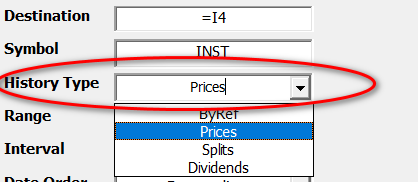

History Type

Range

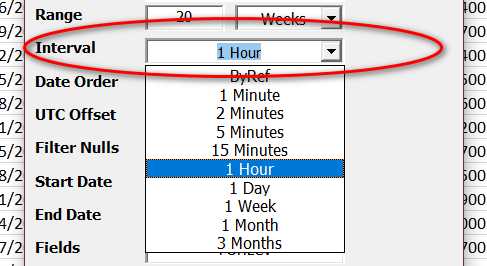

Use the Range part of the dialog to specify the range (the total time span) of the historical data requested. There are two fields; the left-most is numeric and the right-most allows you to specify the units as minutes, hours, days, weeks, months or years. You can also select YTD (year to date) and Maximum. Maximum may give unpredictable results and intervals.

It is possible to request data beyond the limits of what is available from Yahoo, in which case there will be an error reported in the UDF cell. The data limits are approximately:-

Interval

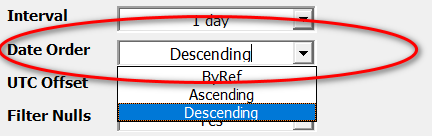

Date Order

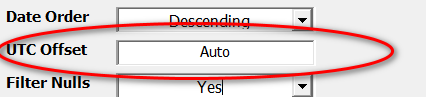

UTC Offset

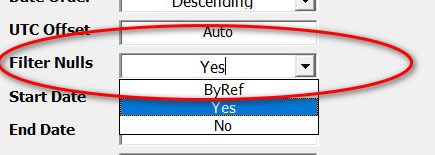

Filter Nulls

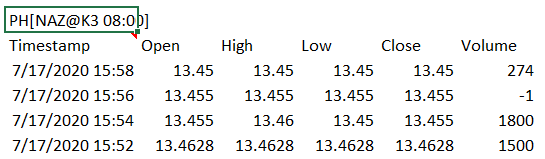

When securities are thinly traded, there can be intervals where no price is set because no trading occurs. The provider returns null prices for these intervals. In this example, with Filter Nulls set to Off, a security NAZ shows no trades for the 15:56 interval:

Setting Filter Nulls to "Yes" will fill the null periods with prices interpolated from the close price of the previous interval. In this example, if Filter Nulls is set to Yes, the data would present like this:

The 13.455 price from the 15:54 interval close is applied across the 15:56 interval, and the Volume set to -1 to indicate an interpolated interval. This processing can improve in both the graphing and numerical analysis of the data.

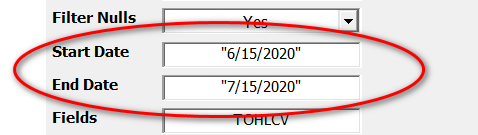

Start Date and End Date

Fields

Headers

Refresh

The PriceOnDate function

Add a Reference to the Add-in

The HP_GetYahooRequest function

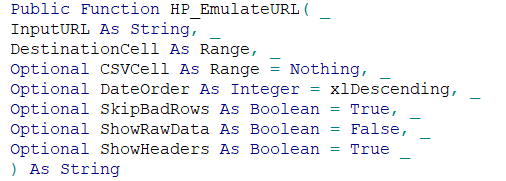

The HP_EmulateURL Function