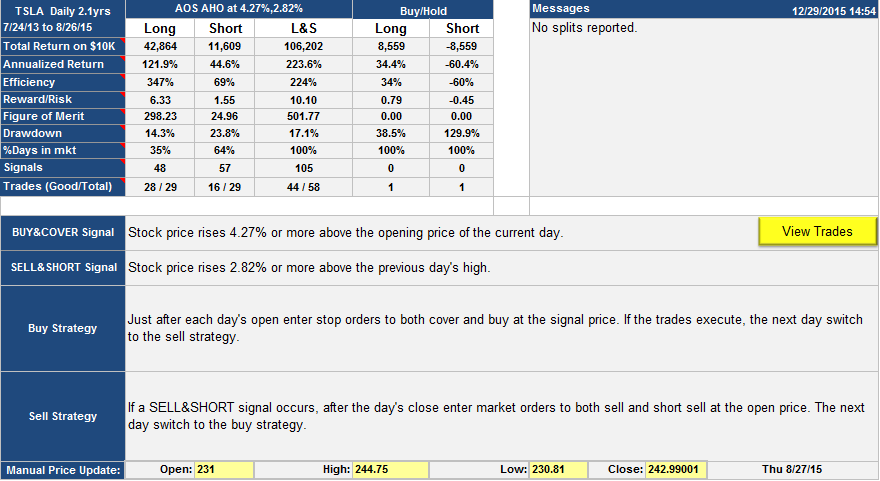

This TSLA trading strategy would have given a 1062% return over 2.1 years vs. a buy-hold return of 86% for the same period. The strategy is based on buying and selling when the stock price rises above specific thresholds. The buy side keyed off the day’s open price; the buy and cover signal appeared when the price rose 4.27% above the open price of the day, and the buy is at the signal price, so you would have to set up stop orders for the buy and the cover.

The sell and short signals came along when the price rose 2.82% above the previous day’s high, and the sell actions occured at the subsequent open using market orders. Every day you would have to recalculate the buy or sell point to find the new buy or sell price. SignalSolver will re-calculate the prices each time you update the prices from the web or enter the latest prices manually. Here is the list of trades.

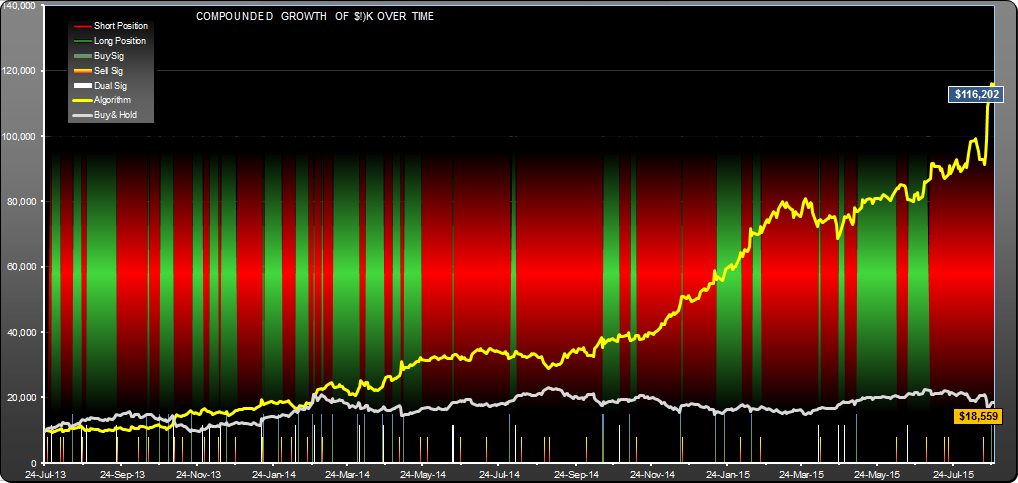

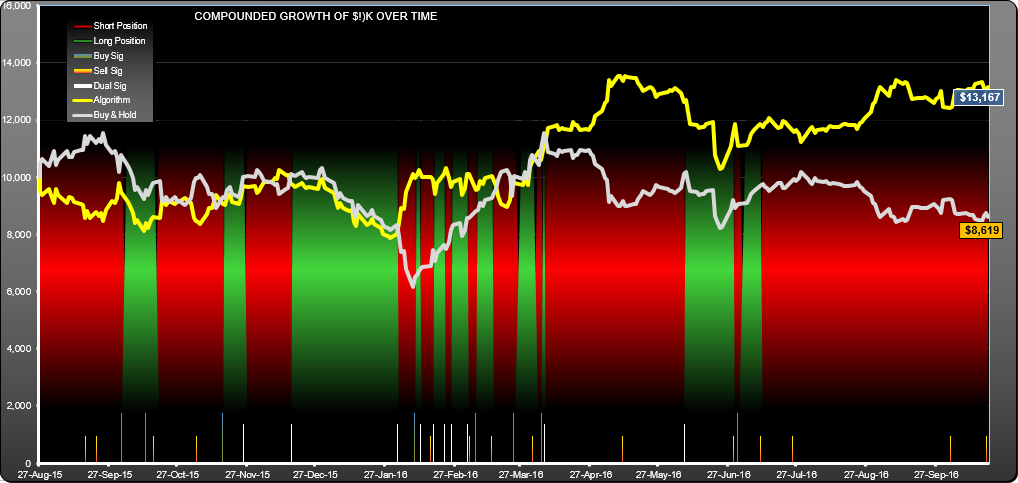

The equity curve shows the return of $10,000 over time for the algorithm (yell0w) and buy-hold (gray):

This algorithm spent 64% of its time short. Looking at the signals at the bottom of the chart, you may notice that they are fairly thin, and there are 21 dual signal days, 28 buy signal days and 36 sell signal days. There is occasional reinforcement of signals, OK but not great.

From the performance table you can see that the long side of the algorithm worked much harder than the short side (the leftmost two columns), but the combination (always being long or short) gave annualized return of 223%.

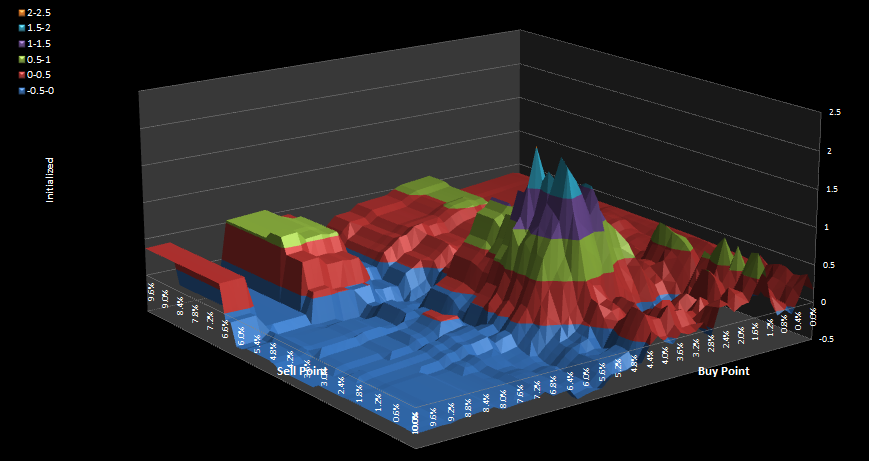

Lets look at sensitivity to the buy and sell parameters.

The dotted line is buy-hold annualized return at 34.45%. The colored lines are the return for different values of buy and sell percentage in different time periods. The blue line is the overall performance for the whole 2.1 year period (528 daily data points), the other green, red, yellow and white lines each represent one quarter of the data (which I call a quartus). As you move the buy or sell point out of the region, you can see that some quartus’s would have been lossy. The worst performing quartus for the chosen buy and sell points was the most recent one, 02/19/15 to 08/26/15, and the annualized return was 161%. The algorithm was found by instructing SignalSolver to find strategies with the best minimum quartus return.

If you map the return for a large range of buy and sell points you notice that the overall surface is a little peaky.

While there is a fair amount of space under the peaks, there are also steep cliffs in the vicinity, so if the buy and sell points were to move around over time you would be in trouble. For that reason I would not expect such high gains in the future.

I will be paper trading this strategy for a while and will post the results from time to time.

Andrew

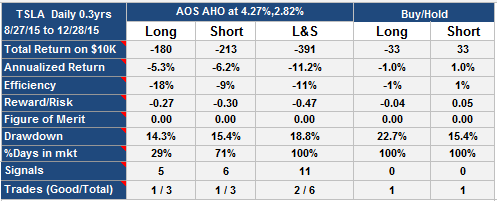

The above analysis has been corrected 12/29/15 for a bug in the short side return.

Update 12/29/2015:

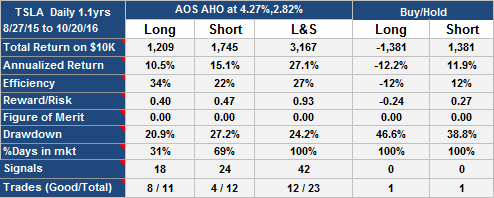

Update Oct 21st 2016

TSLA Trading Strategy (Daily) Update Oct 21st 2016

TSLA Trading Strategy (Daily) Update Oct 21st 2016