Updated 1-2-2016 to correct an error in the short-hold returns.

Update Aug 28th 2015:

Update 2-1-2016

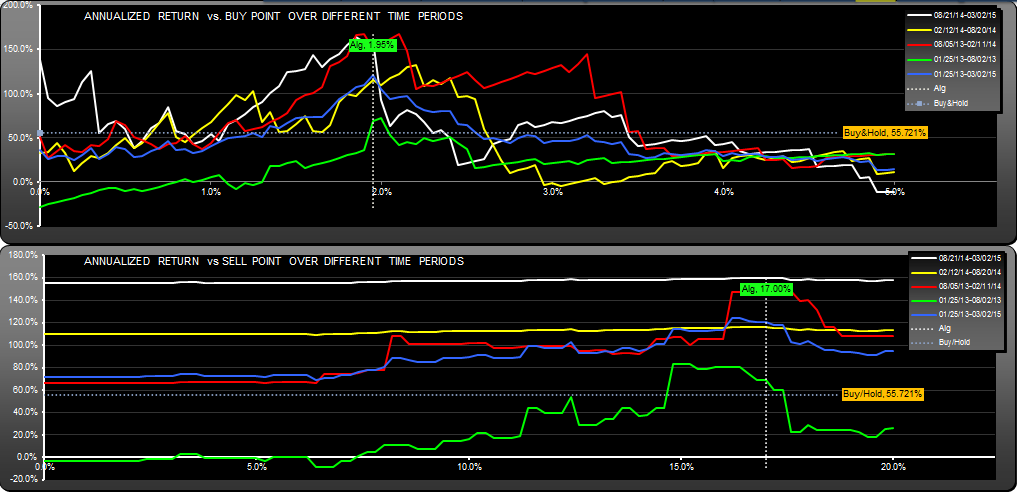

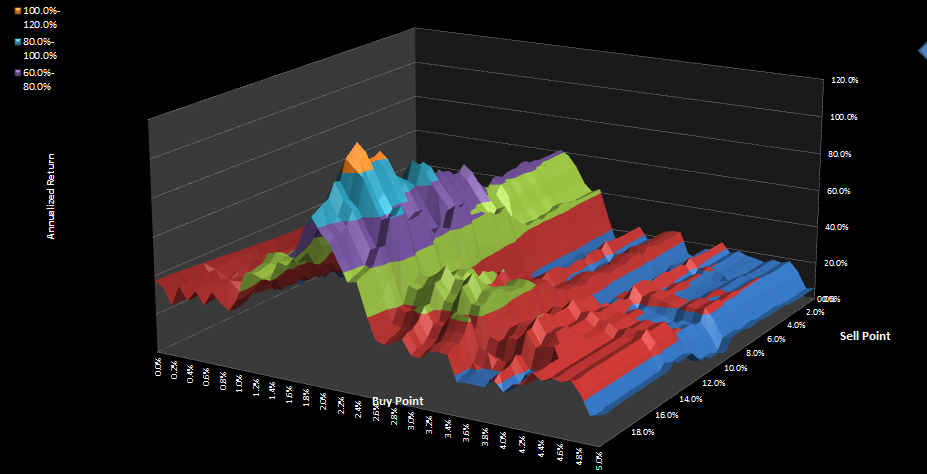

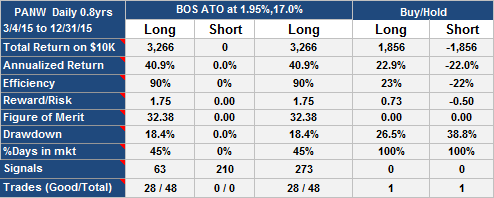

Algorithm has had better return, efficiency and drawdown than Buy/Hold, but not consistently. Optimum buy point dropped to 1.25% (which would have given a return of $4,316)

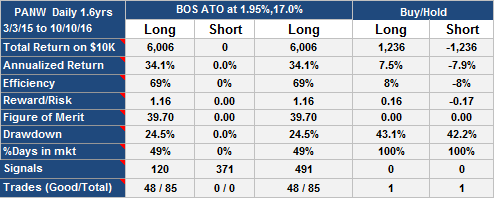

Update 10-10-2016

Algorithm continues to have better return, efficiency and drawdown than Buy/Hold. Buy-hold lost 12% annualized, this strategy made 28.7% annualized. Efficiency (55%) is what the strategy would have made annualized, had the money been invested at the same rate while the strategy was out of the market.

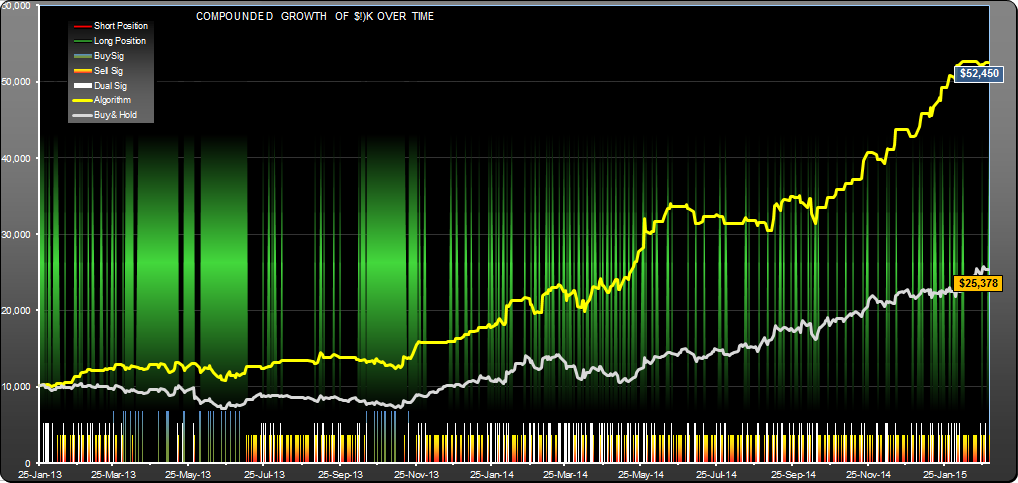

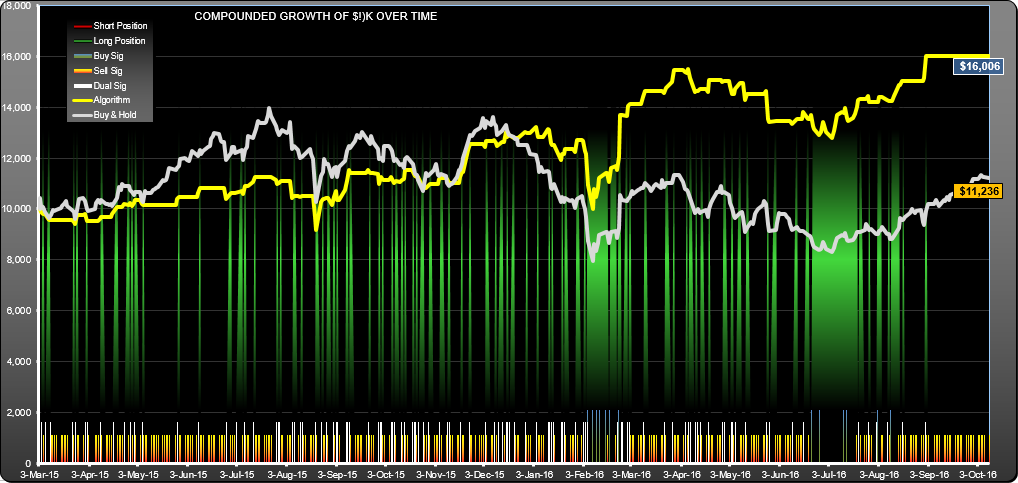

PANW Trading Strategy Performance since publication as of Oct 10th 2016

Here is a view of the performance since original publication in March 2015:

PANW Trading Strategy, performance since initial publication, 60% gain vs 12.3% for buy-hold.

Update 5/26/2015

Since publication on 3/3/2015, the strategy has posted a gain of 1.5% while the PANW stock has posted a gain of 14.56%. There have been 11 trades, 5 profitable.

Andrew

Update 8/28/2015:

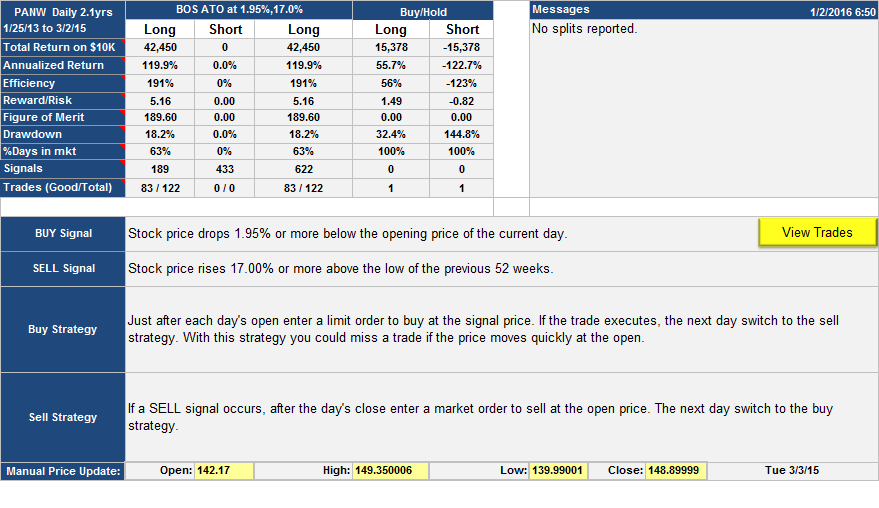

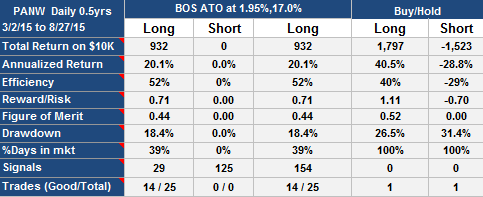

Since the original post on 3/3/2015, the strategy has gained 7.16% with 18.4% drawdown while the stock has gained 12.68% with 26.5% drawdown. The reward-risk for the stock over this period is better than for the algorithm (1.11 vs 0.71). The algorithm was in the market 39% of the time making it a little more efficient than the stock (52% vs. 40%).